Exchanges in name only. They're dark pool prime brokers.

Hey friends -

I've got a bone to pick. Cryptocurrency exchanges are a lot of things. They engage in financing, custody, prime brokerage, and a whole variety of other financial activities.

None are "exchange" activities. Crypto exchanges aren't exchanges.

Calling a firm an exchange that actually engages in a much broader business seems to be innocuous at first glance. But the lazy terminology belies real often poorly managed risks that main street consumers are not well equipped to unpack until it's too late. Look no further than "crypto exchange" Voyager:

Man loses down payment for house when crypto exchange [Voyager] goes bankrupt

It's high time we unpack crypto exchanges.

In this week's letter:

Exchanges in name only, crypto exchanges look a lot more like dark pool prime brokers

A multibillion-dollar crypto bankruptcy, $100 trillion in global GDP, and more cocktail talk

A pre-prohibition drink popular with the East India Company, the East India Cocktail

Total read time: 19 minutes, 51 seconds.

Coinbase is the prototypical crypto exchange. It was a high-flying, venture capital-funded startup before its big-splash IPO in April 2021 ($COIN).

The company made headlines this week (emphasis mine):

BlackRock, the world's biggest asset manager, has formed a partnership with publicly traded crypto exchange Coinbase to make crypto directly available to institutional investors.

Coinbase prime will provide crypto trading, custody, prime brokerage, and reporting capabilities to Aladdin's Institutional client base.

Call me confused. Call me old-fashioned. But that's not what I thought an exchange was. 15 U.S. Code § 78c defines an exchange as:

any organization... which constitutes, maintains, or provides a market place or facilities for bringing together purchasers and sellers of securities

The definition then goes on to expand "facility" to include a broad range of activities including "system[s] of communication to or from the exchange." It's broad, but certainly not so broad as to include custody and prime brokerage.

I've got a feeling we're not in Kansas anymore.

The aberration (abomination?) that is a "crypto exchange" is best understood in the context of what we mean we way say stock exchange. It's a structure that's existed in various forms for at least 400 years starting with the formation of the Amsterdam Stock Exchange.

Nasdaq is one of the largest stock exchanges in the US and is as good an example as any of how one operates. It maintains financial, liquidity, and corporate governance standards that companies must meet to be eligible to list on the exchange. Nasdaq similarly maintains eligibility requirements for who can actually use the exchange, everyone else goes through intermediaries.

Companies that intend to sell shares in the company to the general public can do so through Nasdaq in an initial public offering (IPO) or direct listing. In an IPO, the company creates new shares and sells them. In a direct listing, existing owners in the company are permitted to sell to the general public for the first time.

Most stock exchange activity is composed of secondary trading - trades between existing shareholders in the company. Such activity does not directly involve the company whose stock is being traded. The exchange itself acts as the meeting place - whether virtual or physical - to facilitate the buying and selling interactions.

Note that the exchange is not actually facilitating the trade itself, just the agreement to buy and sell shares in a company. Those instructions are then relayed through a series of parties to actually effect the exchange of shares from seller to buyer and money from buyer to seller.

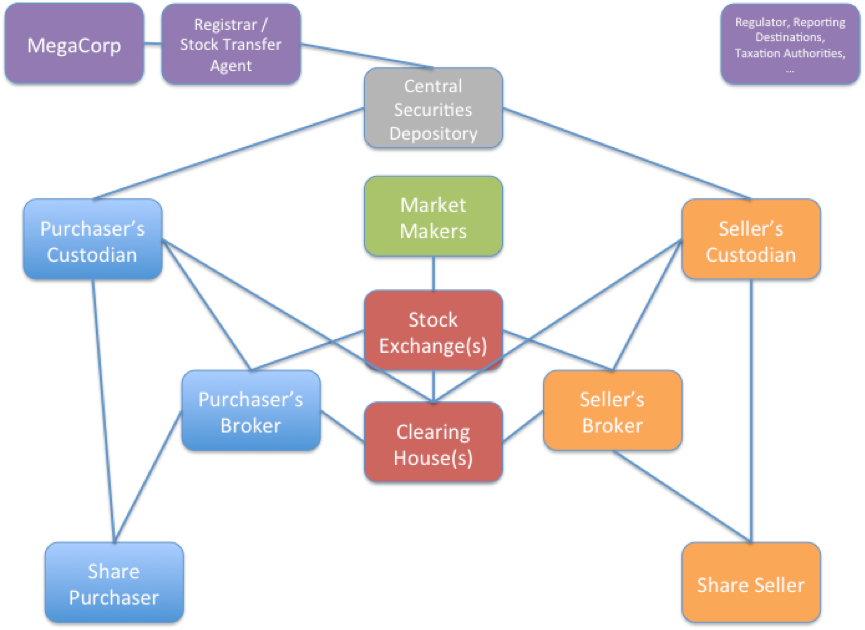

A simplified version of what happens is as follows:

A buyer wishes to buy shares and a seller wishes to sell. Neither buyer nor seller actually holds shares themselves. Instead, their respective brokers hold shares on their clients' behalf at custodians like BNY Mellon or State Street Street.

The buyer instructs their broker (e.g. Fidelity) to buy shares in a company listed on NASDAQ. The seller instructs their broker to sell shares in the same company.

Those instructions are relayed to and matched by NASDAQ.

NASDAQ sends the matched trade to Nasdaq Clearing, although they could in theory send the matched trade to a third-party clearinghouse.

The clearinghouse steps into the middle of the trade - it agrees to transfer shares to the buyer and money to the seller.

The clearinghouse instructs the custodians to transfer money and shares.

The custodians use a central securities depository to execute the transfer. In the US, it's Depository Trust and Clearing Corporation (DTCC).

Lots of messages are relayed across all of the involved parties to notify everyone the trade has been settled.

It's a fragmented and often inefficient process that involves a remarkable number of parties. There's a lot of room for improvement.

But there's also strength in the fragmentation. The party that keeps your shares safe - the custodian - isn't directly involved in the trading activity. The party that matches trades - the exchange - doesn't get involved in exchanging shares and money. The party that takes retail investor orders - brokers - doesn't update the record of who owns what.

The separation of duties, some of which are mandated by regulators, meaningfully reduces risk and the potential for dishonest shenanigans. Take the clearinghouse for example. It only momentarily guarantees a trade - that the buyer will show up with money and the seller will show up with shares. It doesn't have long-term access to shares or money it could pilfer to plug holes elsewhere in its business. The structure forces the clearinghouse to be extremely diligent about who is allowed to use the service and minimizes the opportunities for misusing customer funds.

Or take the broker for example, who is holding shares and cash on behalf of investors. Similar to FDIC insurance at banks, brokers have SIPC insurance that protects up to $500,000 in securities or $250,000 in cash per investor in the event that a broker goes bankrupt. When brokers use clearinghouses to execute trades, they replace buyer/seller counterparty risk - that the other party fails to show up with the money or stocks - with clearinghouse counterparty risk. The clearinghouse is much less likely to fail, further reducing risk for investors.

Or take the custodian who takes instructions from a third party - authorized by a shareholder - to update a record of ownership. It's not involved in trading activity where it could attempt to profit by buying or selling at just the right time, perhaps on the opposite side of its customers' trades.

The fragmentation also reduces information asymmetries. Each of these parties is like one of the blind men touching the elephant - none of them ever see the whole picture of the entire trade lifecycle across all trades. A firm that did could use its information advantage to unfairly profit from those who wished to buy or sell.

It brings us to crypto exchanges. They're all of these parties - and more - wrapped into one.

Coinbase is as good as any crypto exchange to dive into. It's reasonably emblematic of other centralized crypto exchanges like FTX but comes with the bonus that as a public company, it discloses more information than most other competitors.

For clarity - my analysis here is exclusively on centralized crypto exchanges. Decentralized exchanges are their own bundle of fun. Despite the similarity in terminology, the underlying mechanisms and processes - and the risks they present - are materially different. If you're not familiar with decentralized exchanges, fear not - they have nothing to do with what follows.

There are two main ways to break down Coinbase: by customer segment and by legal entity structure. Let's look at both.

There are two main customer segments: retail like you and me and institutional like BlackRock. As a general rule of thumb, products available to retail customers are also available to institutional customers, but products available to institutional are not necessarily available to retail. Coinbase also supports a large ecosystem of third parties who use services like Coinbase Commerce for merchants who want to accept cryptocurrency payments.

In the US, Coinbase is the crypto onramp for retail customers. Users can transfer dollars to their Coinbase account through credit cards, PayPal, wires, and ACH. Once dollars are loaded into Coinbase, they can be exchanged for a variety of tokens. When consumers want to convert back to dollars, they follow the process in reverse - sell tokens for dollars and transfer the dollars back out to their bank or PayPal account.

Tokens held at Coinbase are by default "custodied" at Coinbase. The company's terms state that:

Title to Supported Digital Assets shall at all times remain with you and shall not transfer to Coinbase. All interests in Digital Assets we hold for Digital Asset Wallets are held for customers, are not property of Coinbase, and are not subject to claims of Coinbase’s creditors... Except as required by law, or except as provided herein, Coinbase will not sell, transfer, loan, hypothecate, or otherwise alienate Supported Digital Assets in your Digital Asset Wallet unless instructed by you.

That all sounds proper and above board. Unfortunately, it's directly contradicted by a disclosure in the company's recent quarterly filing:

Moreover, because custodially held crypto assets may be considered to be the property of a bankruptcy estate, in the event of a bankruptcy, the crypto assets we hold in custody on behalf of our customers could be subject to bankruptcy proceedings and such customers could be treated as our general unsecured creditors.

Given the confusion, I have no idea what token "custody" for Coinbase retail customers actually means. The legal entity structure doesn't help, a point we'll return to.

Dollars seem to be more straightforward. Per the company's terms (emphasis mine):

To the extent your USD is held as cash, the balance of your USD Wallet is maintained in pooled custodial accounts at one or more banks insured by the FDIC. Our custodial accounts have been established in a manner to make available pass-through FDIC insurance.

This is the standard and preferred setup for firms pursuing a "rent-a-bank" model. As Seward & Kissel's analysis of FDIC pass-through insurance guidance makes clear, the fact that Coinbase has obtained pass-through insurance sheds a lot of light on how the funds are held (emphasis mine):

for FDIC insurance to “pass through” the agent or custodian to the customer, thereby permitting the customer to be eligible for insurance to the same extent as if a direct account relationship had been established at the Insured Institutions, the parties must have a bona fide agent or custodial relationship, not a debtor/creditor relationship. Furthermore, the custodian’s customer must own the deposit accounts and not merely have a pro rata interest in a pool of deposits.

Coinbase itself curates the list of approved tokens and NFTs for purchase. Only those that it lists can be purchased and sold through Coinbase.

When retail customers trade tokens on Coinbase, they don't interact with a blockchain. Rather, Coinbase maintains large reserves of each of the tokens it lists. Retail trades are settled internally within retail user omnibus accounts. Coinbase either matches buy/sell orders among Coinbase customers or takes the other side of the trade itself. Once a trade is matched, the exchange of tokens and payment is all facilitated internally within Coinbase without connecting out to a blockchain.

Coinbase makes money on the spread - the difference between the buy (bid) and sell (ask) prices - and on transaction processing fees. Fees typically total 1.5% to 3% per trade. When Coinbase takes the other side of a trade, it can make additional money as a prop trader - selling tokens at a higher price than it bought them for.

Note already the difference between this crypto "exchange" and what we typically expect from an exchange. Everything from the moment a customer loads dollars into the system through to when they take their dollars back happens internally within Coinbase. There is no separation of responsibilities among parties and no Chinese firewalls to prevent data from being shared across all business lines. The same company that trades with its own money also custodies customer funds.

Alongside the core "exchange" service, Coinbase also offers several other, ancillary products including:

Coinbase Wallet - tokens are bearer assets. Whoever owns the cryptographic keys, owns the tokens. A wallet stores cryptographic keys. Coinbase Wallet allows users that don't want to custody their tokens at Coinbase or who purchase tokens outside the Coinbase exchange to self-custody their tokens.

Coinbase NFT - similar to the company's core offering, Coinbase recently launched an NFT marketplace. In an interesting shift, users must self-custody their NFTs using Coinbase Wallet or another crypto wallet of their choosing. Trades in the NFT marketplace do interact directly with the blockchain and the company currently does not collect any fees as it tries to ramp up marketplace trading volume.

Advanced Trade - similar to the company core's offering, Advanced Trade adds on a bunch of bells and whistles like lower transaction fees (~0.5%) and technical charting to encourage more trading. Users can also earn up to 5% yields on select tokens, although the details on how those yields are generated are not entirely clear. Coinbase collects an unspecified commission on yield.

Coinbase Borrow - borrow up to $1 million against Bitcoin held at Coinbase, up to 40% of the value of your Bitcoin holdings. The company charges interest on the loans, starting at 8% APR.

The first rule of investing and trading is don't lose money. It's something that clients of Bernie Madoff forgot to disastrous effect. Even above and beyond regulatory requirements that enforce protections for money managers working on behalf of retail investors, institutional customers like BlackRock demand clear and unambiguous asset custody.

Coinbase Custody is the service that provides those needed guarantees via in-house custodian Coinbase Custody Trust Company. As a qualified custodian, it holds assets in separate accounts in the customers' names. There are many restrictions on what the company can do including prohibitions on its ability to take on debt or other contractual obligations that could result in competing claims on customer assets. In short, it's a structure that's purposefully designed such that customer assets are unambiguously the property of the customer - not Coinbase - in the event of a Coinbase bankruptcy.

The service is insured for up to $320 million, although the exact details of what the insurance covers aren't public. Of the $278 billion stored with Coinbase as of December 2021, it appears that between 10% and 20% is custodied with Coinbase Custody.

The company's done its best to obfuscate custody fees. The pages that were previously linked to fees now redirect to information that's entirely unrelated or simply don't work. Thankfully a previous version of the page has been archived - the minimum balance is $500,000, one-time "implementation fees" range from $0 to $10,000, and ongoing fees average 0.50% per year.

Coinbase Custody is the foundation of Coinbase Prime, the primary institutional offering. Prime is short for prime brokerage, a generic catchall term for the bundled services that investment banks often offer hedge funds and family offices. Standard services include over-the-counter trading for large trades and borrowing facilities that enables the investor to purchase, short, and otherwise trade on a netted basis.

The last part - borrowing facilities - are particularly interesting. As a retail customer, if I want to buy $100 of Bitcoin, I have to load $100 onto Coinbase and then purchase $100 of Bitcoin. But if I'm an institutional customer with Prime, I can instruct Coinbase to purchase $100 of Bitcoin on my behalf using Coinbase's capital. If we agree to settle daily and the value of the Bitcoin falls to $95 by settlement time, then I owe Coinbase $5 plus the interest on the $100 loan.

Coinbase gets paid for taking on the risk that I fail to pay them back and the price movement risk. I'm willing to pay for the service because I retain control over my $100 rather than having it locked up in a trade at Coinbase.

Alongside Prime, Coinbase also sells vast reams of data. Everything from tick level data through details on the full order book can be bought and streamed. Given that there are few restrictions on the company's ability to sell data and the remarkable breadth of data retained by the company owning the entire trade lifecycle, it's probable that "unlisted" data is available to preferred institutional users.

A quick glance at Coinbase's annual report reveals the nature of their business: 95% of revenue is generated from retail customers despite retail generating only 35% of the transaction volume.

It's a pattern reinforced by other company activities:

The $480 million in revenues from trading against clients generated a 10% net operating profit.

Key company executives and family members generated $29 million in trading revenues for Coinbase. The company didn't disclose what information they used when making the trades.

In short, Coinbase is a highly effective wealth transfer program - from retail to institutional. It's a pattern representative of most centralized crypto exchanges.

The Coinbase parent company is regulated on a per-state basis as a money services business (MSB), the same structure used by PayPal. Coinbase Custody Trust Company is a subsidiary that's structured as a New York limited purpose trust company and acts as a qualified custodian.

MSB regulations were written to govern actually money movers like Western Union. The regulations are notoriously inadequate for the types of companies that now qualify as such including PayPal and cryptocurrency exchanges. From my earlier piece Bad Money Rising:

At the time I wrote that, pulling from an analysis done by Dan Awrey, PayPal stored about $35 billion in customer funds as "direct claims" against PayPal. That's corporate speak for saying PayPal customers are general unsecured creditors. In the event of bankruptcy, there's a real probability they are stuck in line alongside the other lenders hoping to get their money back. Worse, as general unsecured, they're likely at the bottom of the pecking order.

As of December 2021, Coinbase stored $10.5 billion in "Customer custodial funds." It's a rather weird and ambiguous balance sheet line item. Custodied funds are not traditionally included on the balance sheet. Bank of New York Mellon - the largest custodian in the world - leaves it off its balance sheet. PayPal also leaves it off and is explicit about it: "Customer funds for which PayPal is an agent and custodian on behalf of our customers are not reflected on our consolidated balance sheets."

Coinbase goes to some lengths to try to reassure readers that the funds are safe (emphasis mine):

We had customer custodial funds of $10.5 billion which consisted of amounts held at certain third-party banks for the exclusive benefit of customers... Certain jurisdictions where we operate require us to hold eligible liquid assets... equal to at least 100% of the aggregate amount of all custodial funds due to customers... As of December 31, 2021 and December 31, 2020, our eligible liquid assets were greater than the aggregate amount of custodial funds due to customers.

Not only can Coinbase optimize the states in which they store customer funds to minimize the amounts it has to hold on behalf of customers, but even the most onerous state requirements are woefully inadequate. "Customer custodial funds" feels more like a turn of phrase intended to give reassurance without any actual substance. Certainly, the company could make more money if they had free use of customer funds, a practice that wouldn't be unsurprising given how they already generate the vast majority of their revenues.

Without more information, it's impossible to know how Coinbase retail customers would be treated in bankruptcy. Especially in an industry as fraught with fraud as crypto, you would expect a company that takes protecting user funds seriously to be flaunting its structure. The endless obfuscation is not promising.

All of this stands in notable contrast to the qualified custody services offered to institutional customers via Coinbase Custody Trust Company. Those funds are properly bankrupt remote.

It's difficult to know precisely what terms govern the use of Coinbase Custody and Coinbase Prime - the user terms are not publicly available. But you can be reasonably assured that a firm like BlackRock went through every single line to ensure that their customer funds would be protected no matter what happens to Coinbase. Those guarantees don't exist for retail customers.

The conclusion is troubling. It appears that Coinbase's legal entity structure is structured similarly to the overall business - retail customers take on significant and unnecessary risks when using the services, risks that the company has mostly eliminated for institutional users. It's almost worse knowing that the company can eliminate the risk and chooses not to than if they treated all customers equally poorly.

I'm a little concerned that I may be accused of unfairly bashing Coinbase, so let me be clear. Almost every centralized crypto exchange exhibits similar rampant abuse of retail users and obfuscation of what they're actually doing.

A smattering of examples will suffice:

Voyager repeatedly and publicly claimed that customer funds were FDIC insured. They weren't. The company recently filed for bankruptcy.

The President of FTX stated that "stocks are held in FDIC-insured and SIPC-insured brokerage accounts." Brokerages and stocks are not eligible for FDIC insurance.

Binance offered and marketed its services across the UK despite not holding "any form of U.K. authorization, registration or license to conduct regulated activity in the U.K."

I'm glad we got that cleared up.

Crypto exchanges are exchanges in name only.

Bringing together buyers and sellers is just a small part of what they do. The vast majority of their business is made up of the many activities that are deliberately separated out into separate companies for securities trading - asset delivery, settlement, representing retail customers, custody, borrowing, lending, and more.

It's a business model not lost on regulators. Lael Brainard, the Federal Reserve Vice Chair, highlighted the problem in a recent speech:

We have seen crypto-trading platforms and crypto-lending firms not only engage in activities similar to those in traditional finance without comparable regulatory compliance, but also combine activities that are required to be separated in traditional financial markets. For example, some platforms combine market infrastructure and client facilitation with risk-taking businesses like asset creation, proprietary trading, venture capital, and lending.

Any hypothetical cost advantages that might be gained by combining the many disparate activities under a single roof are overwhelmed by the already realized predatory pricing and woeful risk management. Even the very basics of how traditional financial services firms protect custodied client funds are being ignored when it's profitable to do so.

It's clear that "exchange" is a poor term for what these crypto companies are actually doing. Maybe we should instead just call them what they are - a bad idea.

If that doesn't catch on, "dark pool prime broker" is a better fit. Dark pools are off-exchange securities trading venues where trades are confidential, outside the purview of the general public. Coinbase and other crypto "exchanges" have essentially taken that model and bundled it with traditional prime brokerage but for crypto.

Dark pool prime broker is also a term that feels like what it is - less regulated, less reputable, and ultimately less trustworthy.

I'd love to tell you that my conclusions are novel and that this letter will be the catalyst for major change. I'm not that optimistic. Rather, I'm somewhere around the fourth stage of grief - past anger and onto depression.

Just read the key findings from the Office of the New York State Attorney General from 2018:

The Various Business Lines and Operational Roles of Trading Platforms Create Potential Conflicts of Interest. Virtual asset trading platforms often engage in several lines of business that would be restricted or carefully monitored in a traditional trading environment... Additionally, platform employees – who may have access to information about customer orders, new currency listings, and other non-public information – often hold virtual currency and trade on their own or competing platforms.

Trading Platforms Have Yet to Implement Serious Efforts to Impede Abusive Trading Activity. Though some virtual currency platforms have taken steps to police the fairness of their platforms and safeguard the integrity of their exchange, others have not... Those factors, coupled with the concentration of virtual currency in the hands of a relatively small number of major traders, leave the platforms highly susceptible to abuse.

Protections for Customer Funds Are Often Limited or Illusory. Generally accepted methods for auditing virtual assets do not exist, and trading platforms lack a consistent and transparent approach to independently auditing the virtual currency purportedly in their possession; several do not claim to do any independent auditing of their virtual currency holdings at all. That makes it difficult or impossible to confirm whether platforms are responsibly holding their customers’ virtual assets as claimed. Customers are highly exposed in the event of a hack or unauthorized withdrawal.

How you might ask, did the Attorney General come to such conclusions? By sending voluntary questionnaires to dark pool prime brokers. The conclusions are all based on data the crypto companies provided.

To come to the same conclusions four years later - almost to the month - is disappointing.

There are crypto companies doing great work - digitizing money, improving stock settlement, rethinking music streaming to return more to artists, making video game loot fully transferable across games, and more. But the shenanigans perpetuated by bad actors - especially the large, prominent dark pool prime brokers - are overshadowing their good work.

Despite my momentary depression, I remain overwhelming hopeful. It takes time to build right, but it's a model that will win out in the end. Every day, I meet with crypto companies who are looking out for their users and treating them fairly. I look forward to the day when the dark pool prime brokers have gone the way of the dinosaurs and the good guys take their place in the limelight.

Three Arrow Capital, a cryptocurrency investment firm, is in bankruptcy. The founders are on the lam. The supposedly conservatively managed firm was in fact massively leveraged and likely was insolvent many months before it formally declared bankruptcy. Coming in at over 1,100 pages, the bankruptcy filings are intimidating but offer an unprecedented look at how such a firm can operate and build multi-billion dollar positions. Frances Coppola went through the filing in its entirety and distilled it down. (Coppola Comment)

For all the talk about crypto reinventing finance, we seem remarkably determined to make the same mistakes again and again. Axie Infinity, a blockchain-based game, was hacked earlier. Players lost over $540 million. Despite the remarkably large losses and involvement of North Korea as the hacker, there's not a lot about the hack that's crypto-specific. It was good-old social engineering. An Axie Infinity engineer was emailed a PDF for a fake job offer. They downloaded it onto Axie Infinity systems. Poor internal controls combined with poor security practices allowed the hackers to wreak havoc. (The Block)

The world's on track to top $100 trillion in global GDP for the first time this year. With all the daily news and political noise, it's easy to lose track of scale. Visualizations help. The US is 15% bigger than China which is 4x bigger than Japan, the third largest economy. With few exceptions, size rapidly falls off from there. (Visual Capitalist)

Idealogical battles are at the forefront of finance today. Multiple major firms - BlackRock most notably among them - have taken strong stances not to invest in coal and other industries misaligned with ESG (environmental, social, governance) missives. In response, West Virginia just banned five major financial firms from doing business with the state and Florida's governor looks set to pursue a similar approach in the name of not "discriminating against customers for their religious, political or social beliefs." I expect these people would cheer Mastercard and Visa's recent decision to suspend business with the advertisement arm of MindGeek, the largest pornography business in the world. It's a weird world where politicians and voters alike attempt to squash practices they don't like in the name of anti-discrimination. (NY Times, Reuters)

A warm weather sipper from India in the 1800s.

2.0oz Pierre Ferrand 1840 Cognac

1tsp Cointreau

1tsp Rich Pineapple Syrup

2 dashes Maraschino Liqueur

2 dashes Angostura Bitters

Pour everything into a mixing glass. Add ice until it comes up over the top of the liquid. Stir for 20 seconds (~50 stirs) until the outside of the glass is frosted. Add ice to a rocks glass. Strain in cocktail and enjoy!

A pre-prohibition cocktail popular with the East India Company Brits in India. With my melting candles giving you a glimpse of the temperatures here in New York, I felt right at home with this hot weather drink. As much as I enjoy it, I'm not going to defend it as a good cocktail. It's a bit like someone wanted cognac but didn't want to drink it straight. So they tried some additional orange notes. That didn't quite meet their desire, so they tried some spice. Then some sweet. Then some savory. At no point did they ever consider pouring the damn thing out and starting over rather than repeatedly adding just a little bit more of that one last thing. The result is a hotdog with ketchup and mustard and relish - it works, but you probably shouldn't be proud of it.

Cheers,

Jared