Circle USDC, Paxos USDP and BUSD, and Tether USDT are worth over $100B collectively as the leading stablecoins. But they're not all made equally.

Hey friends -

The world's changed a lot since we looked at stablecoins in October 2021. Algorithmic stablecoins have largely failed, asset-backed stablecoins are faltering, and cash-backed stablecoins are winning out.

Cash-backed stablecoins are entering a new phase of maturation. Broad adoption within the crypto world and increased regulator focus has forced serious competition among issuers.

We're down to three real contenders: Circle (USDC), Paxos (USDP, BUSD), and Tether (USDT). Each is competing with a different business model. While there's been much good discussion about each of the issuers, there have been few attempts to answer the critical question:

If you're a consumer looking to convert $1 USD into a stablecoin, which one should you use?

In this week's letter:

Which stablecoin should you choose?

The origins of the Black Death uncovered, the end of sickle cell anemia, and more cocktail talk

Ned King's Gem, a wonderfully pineapple take on the Daiquiri

Total read time: 12 minutes, 6 seconds.

Cash-backed stablecoins are on the rise. It's a welcome development.

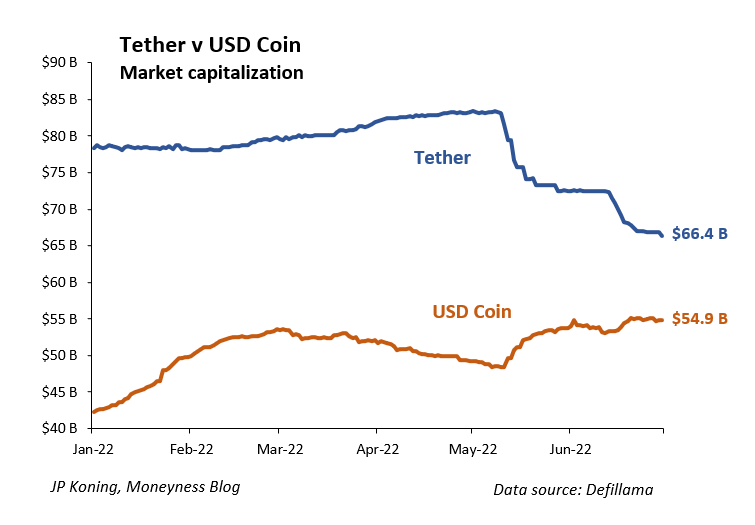

There are three major supposedly cash-backed stablecoin issuers: Circle (USDC), Paxos (USDP, BUSD), and Tether (USDT). Tether has the largest market cap at $66 billion followed by USDC at $55 billion. Paxos's two stablecoins together have a market cap of $18 billion. Collectively, we're talking over $100B in digital tokens that are supposed to stay pegged to $1 USD.

Not all three are made equal. It's clear that in recent months - since TerraUSD blew up and shook holders' confidence in all stablecoins - that USDC has been winning.

The three are in hyper-competition, each issuing stablecoins under a different business model. For any consumer, there are seven key considerations:

Availability - can I easily purchase the stablecoin?

Redeemability - what is my ability to redeem the stablecoin for US dollars in good times and bad?

Stability - these are claims issued by private companies, not fiat money. Do they hold their peg to the US dollar?

Solvency - how strong is the balance sheet that backs the stablecoins?

Transparency - how certain am I of the assets backing the stablecoin and the issuer's risk controls?

Bankruptcy - in the event of issuer bankruptcy, what happens?

Ownership - what is the ability of a third party, government or otherwise, to seize my stablecoins?

There's not a lot of differentiation on availability. Making the stablecoins generally available has been a priority for all three issuers.

The easiest way to buy Circle's USDC and Tether's USDT is through the major, regulated crypto exchanges including Coinbase and FTX. Wire money from your bank account to the exchange and purchase the stablecoin. Some exchanges, like Binance, also let you purchase with a credit card. The exchanges are generally regulated as money services businesses, the same regulations that govern PayPal.

Paxos is also generally available but a little different. The easiest way to buy USDP is through a similar process on their website, fewer exchanges list USDP. BUSD is the default stablecoin for the Binance exchange and can be purchased there. Unlike the exchanges, Paxos is regulated as a National Trust, a new type of bank charter issued by the OCC.

There are real, material differences among the issuers. Circle is free and convenient, Paxos follows behind with wire fees and less convenience, and Tether is functionally unusable for everyday consumers.

Circle's USDC is primarily redeemed via Coinbase. Users can convert USDC to cash and then transfer the cash to their bank account for free using ACH. If users want their money faster, they can pay a 1.5% fee up to a $150 max to receive their money instantly. Withdrawals are limited to $500,000 per day. There are no minimums.

Paxos's USDP is redeemed via Paxos's website. The company no longer supports ACH withdrawals so all redemptions are executed as more expensive wires. The company charges a $20 fee per withdrawal in addition to whatever incoming wire fees your bank charges. Withdrawals are limited to $1 million per day. The minimum is functionally whatever the fee total is.

Tether is difficult to redeem. You have to have an account with the company, which requires a one-time $150 "verification" check. It's the only company I'm aware of that charges such a fee. Tether also charges a withdrawal fee - the greater of $1000 or 0.1%. The minimum withdrawal is $100,000 and even that is sometimes subject. Tether has repeatedly lost access to banking partners and struggled to process withdrawals from time to time.

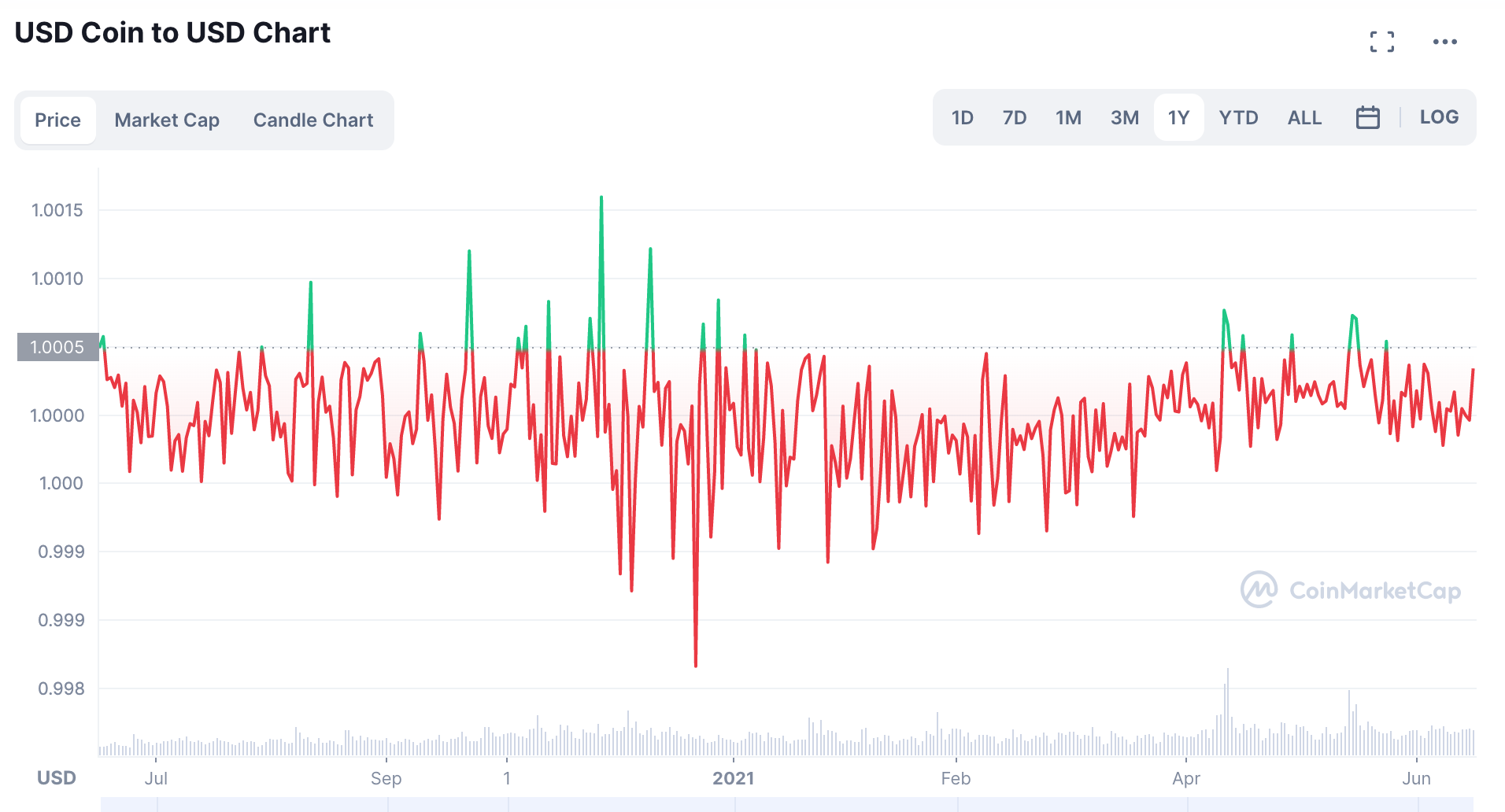

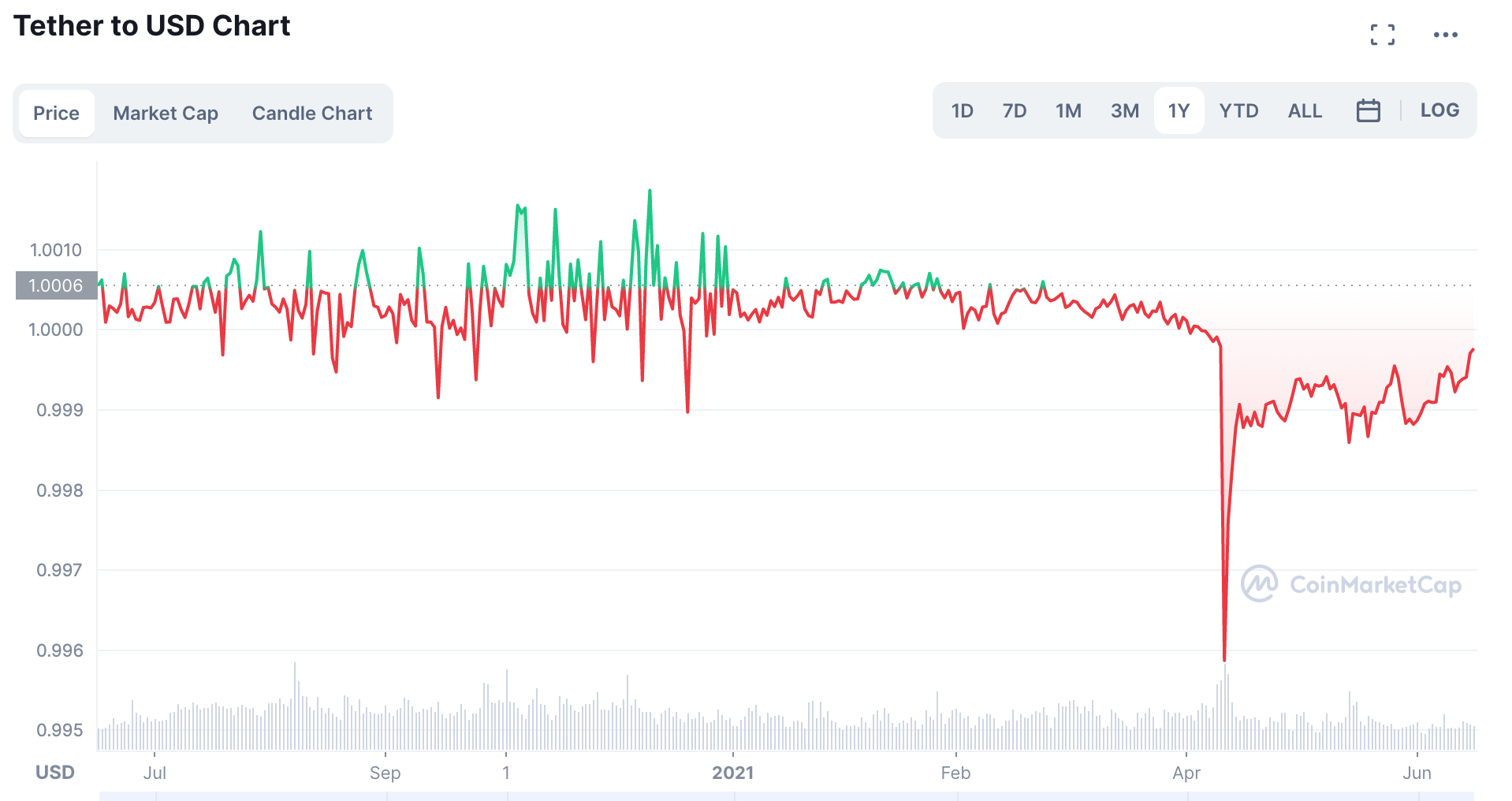

All did a decent job staying pegged to $1 USD in 2021. As market conditions have gotten tougher, Paxos stumbled and recovered. Tether's still stumbling.

Circle's USDC has stayed in the tightest range, generally between $1.0000 and $1.0005. At the extremes, it fluctuated between $0.9985 and $1.0015.

Paxos's USDP has struggled to maintain as consistent a peg. While the stablecoin generally stayed between $0.9990 and $1.0010 through most of 2021, its typical range has more than doubled as market conditions have become more difficult this year. At the extremes, USDP has fluctuated between $0.9950 and $1.0060.

Paxos's BUSD has similarly struggled although less so. It's consistently ranged between $0.9990 and $1.0010 with only the occasional breakout to the extremes of $0.9980 and $1.0035.

Tether has struggled immensely since April - the peg's broken. Before April, Tether maintained a relatively tight range between $0.9990 and $1.0010. Since mid-April, Tether's remained depressed below $1.000. It bottomed at a low of $0.9960 and has mostly traded around $0.9990.

There are two major inputs to stability - market cap and redeemability. Bigger stablecoins tend to be more stable because larger market participants can move significant money in and out, including for any arbitrage opportunities where they can buy stablecoins trading at less than $1 USD and redeem them for cash.

Redeemability is the gating factor - fees and slow redemption reduce the profitability of arbitrage opportunities. Tether's current $0.9990 value is clear evidence - that's the magic number below which arbitrage becomes profitable.

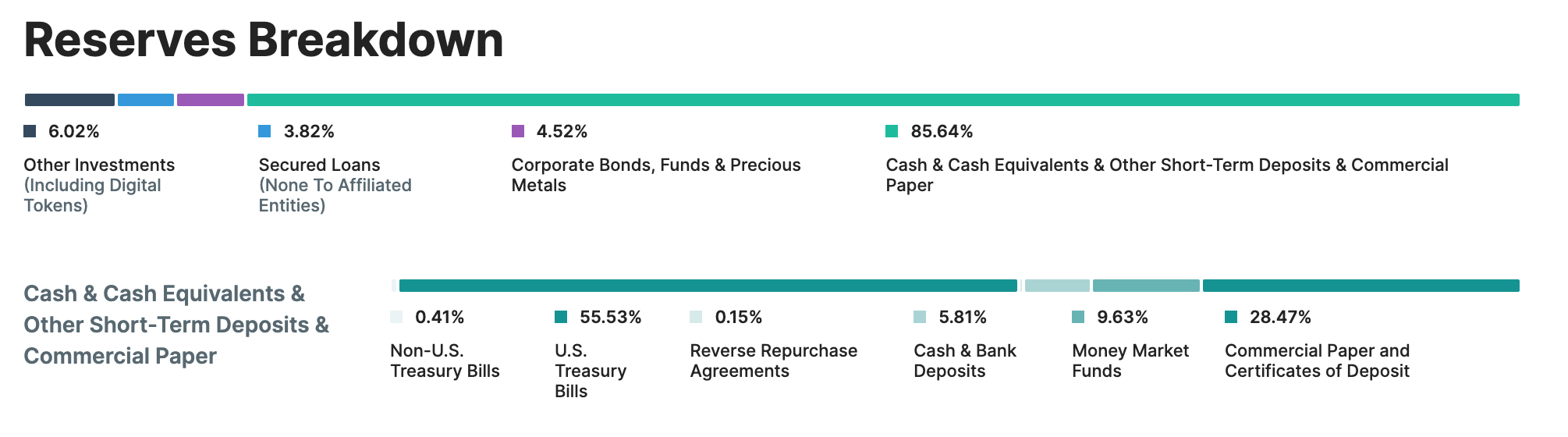

Solvency and Transparency are where the stablecoins truly start to differentiate. I include both under the same header because it's difficult to consider solvency without verifiable knowledge of the assets that back the stablecoins. Circle and Paxos are strong. Tether is a disaster.

Solvency considers the value of the assets that back the tokens. The tokens issued by Circle and Paxos are backed by a mix of US dollars and US Treasuries with less than 90 days maturity. Tether is backed by a whole mess of stuff.

Given the asset mix, Tether looks more like a fund manager than a stablecoin.

Transparency helps us understand if the assets backing the tokens are at least as valuable as the tokens issued. Audits and attestations both help. At the current time, based on the information available, all three tokens are fully backed. The challenge is if the information is accurate.

Circle and Paxos are both subjected to regular annual audits. Circle released theirs as part of the company's plan to go public later this year. Paxos is required to undergo annual audits per NY Department of Financial Services requirements and provides them on a request-only basis. Tether was fined $41 million for falsely claiming they were audited. Flying in the face of the company's many reassurances, there's no evidence the company has ever or will ever be audited.

All three issuers do provide independent, auditor-conducted attestations on the reserves. The attestations verify if the value of the reserves are consistent with the value of the tokens outstanding. Attestations do not test the operating controls, namely how the issuer governs itself to prevent mistakes and fraud. Circle and Paxos work with brand name auditors and release attestations monthly. Tether releases its attestations quarterly, fired its previous auditor in early 2021, and currently works with a nobody whose parent company is being investigated in the UK.

J.P. Koning highlights three keys to transparency:

Timeliness - is the information about the tokens promptly released or do I have to wait to find out if there is a problem?

Completeness - how fine-grained is the information provided?

Trustworthiness - can I trust the audit and attestation process?

The NY Department of Financial Services (NYDFS) has the highest standards for issuance in the country. Paxos is the only one of the three issuers whose stablecoins are regulated by NYDFS. The company is required to publish monthly attestations no later than 30 days after month end and disclose the asset classes of what backs the tokens. Furthermore, auditors are required to test Paxos's internal controls at least once a year.

These are all new requirements as of this month. Paxos is mostly out in front of them. The company releases its monthly attestations promptly and now details the exact breakdown of its stablecoin reserves down to the CUSIPs of the treasuries. The controls testing is to come.

Circle, although not regulated by NYDFS, has largely gone toe-to-toe with Paxos on transparency. In addition to timely monthly attestations, the company also details the weekly aggregate reserves and changes in circulation (issuances and redemptions). In response to Paxos's monthly detailed reserve disclosures, Circle now does the same. It's as yet unclear if Circle will subject itself to the same control testing as Paxos, but the question may be moot. Similar audits may already be required once the company goes public.

Tether hasn't announced any plans to test controls. I doubt they will.

Bankruptcy is where the fun begins. We're venturing beyond published, audited statements and into scenario hypothesizing where we have few to no cases to guide us.

What happens if an issuer goes bankrupt?

Dan Awrey, Professor of Law at Cornell Law, suggests breaking bankruptcy risk into two parts:

Losses stemming from the application of substantive bankruptcy rules. Are the assets backing the stablecoin - the reserves - for the exclusive benefit of the stablecoin holders or are there competing claims?

Temporary illiquidity due to the bankruptcy process. How much time will pass before money is returned to the stablecoin holders?

We addressed the third question of whether there are enough reserves to make stablecoin holders whole under Solvency and Transparency.

Paxos and Tether are both straightforward for opposite reasons.

The most robust way to protect the reserves is in a trust for the exclusive benefit of the stablecoin holders. In bankruptcy, the trust is carved out from the rest of the issuer's estate. It's the structure Paxos supports as required by the company's stablecoin regulator, the NYDFS. There's no substantiative debate here that the Paxos stablecoin holders are exclusively entitled to the reserves. In bankruptcy, funds should be returned quickly.

Tether exists at the other end of the spectrum. In short, it's not regulated. The slightly longer answer is that the company has repeatedly claimed to be regulated but isn't. What happens in bankruptcy is anyone's guess.

Circle is where bankruptcy gets interesting. The company is regulated as a money transmitter on a state-by-state basis, just like PayPal. The good news is that we've had relatively few money transmitter bankruptcies. The bad news is that we've had relatively few money transmitter bankruptcies.

Circle states that the assets backing the USDC stablecoin are in "segregated" accounts for "the exclusive benefit" of USDC holders. Those accounts are omnibus structures without regard to customer jurisdiction. Furthermore:

In the unlikely event that USD in circulation exceeded the value of assets held in segregated accounts, our investment policies and obligations under money transmitter laws would require the Company to immediately increase the amount of unencumbered permissible investments under the control of Circle Internet Financial, LLC to satisfy any shortfall.

Only 28 states require money transmitters to use trusts for customer assets. Circle's setup doesn't sound like a trust and I can't find mention of trusts elsewhere. My working assumption is that Circle's reserves are held in other structures.

It leaves us to fall back on money transmitter bankruptcy cases. Adam Levitin, Professor of Law at Georgetown University Law Center and an expert on bankruptcy and financial regulation, has this to say on money transmitters:

We're in the realm of well-reasoned speculation.

Adam went on to detail the most probable outcome given the information available today:

I think the takeaway is that bankruptcy courts will honor state law property entitlements like express trusts, but they may impose some limits on them.

The caveat here is that many of the express trusts created under money transmitter laws are written as "ipso facto" clauses, meaning the trust is created when the money transmitter declares bankruptcy. Adam highlights that "[i]pso facto provisions that remove property from the debtor's estate don't hold up in bankruptcy."

It means that even if Circle's reserves were held in trusts per one of the 28 states' requirements, we lack clarity on what could happen.

These aren't Circle specific issues, rather they're money transmitter issues. My takeaway for Circle is perhaps simpler than the above messiness would imply. Circle's setup is not materially different from PayPal's. If you're comfortable using PayPal and other companies that are regulated as money transmitters, then Circle's setup is robust.

Ownership is only rarely discussed, but it remains a hugely important conversation.

The cash in your pocket is yours. Your stablecoins are only mostly yours. All three issuers can freeze your tokens.

Circle reserves the right to “block” certain USDC addresses and, if such addresses are Circle custodied addresses, freeze associated USDC (temporarily or permanently) that it determines, in its sole discretion, may be associated with illegal activity or activity that otherwise violates these Terms.

We may freeze, temporarily or permanently, your use of, and access to USDP and/or BUSD or the US dollars backing your USDP and/or BUSD, with or without advance notice, if we are required to do so by law, including by court order or other legal process.

Consistent with the rest of the discussion, Tether's terms are not helpful here. But the company has frozen tokens and accounts before, functionally demonstrating that they have the capabilities and willingness to do so.

This worries me immensely, but it's not a topic to be resolved by any one of the issuers. It's a microcosm of the tension between the freedom to transact and the ability of law enforcement to go after terrorists, pedophiles, and all other variety of bad guys. The politician's cry of eroding freedoms "for the children" is insidious. The costs of the freedoms we give up are only obvious in hindsight.

Circle and Paxos's stablecoins are robust. Tether is nothing short of a disaster, a digital "trust me" slip of paper issued by an unknown entity domiciled in an unclear jurisdiction.

A reasonable consumer could debate the competing virtues of Circle and Paxos's stablecoins. The score would change month to month as each pushes the other to be ever more regulated, more transparent, and more stable.

It's the best of how a competitive market should work - two issuers, competing with each other to create the higher quality stablecoin. Quality isn't a destination but a journey of continual improvement. Circle and Paxos are both on the path and we consumers will be the beneficiaries.

Despite being the most deadly pandemic of all time, the origin of the Black Death has remained a mystery for 700 years. Until now. Researchers traced the plague back to a single village in modern-day Kyrgyzstan where the original parent strain split into four, one of which became the Black Death. (NPR)

Sickle cell disease may be going the way of polio. In a major win for CRISPR, a trial group of 75 patients was administered a one-time treatment to alter the patients' own cells to produce the kind of not-distorted hemoglobin found at birth. All but two of the patients were cured entirely. The conditions of the remaining two were significantly improved. (FreeThink*)

Among consumer packaged goods companies, Unilever is practically in a league of its own when it comes to environmental track records. Just a few years after "accidentally" burning Indonesian rainforest to plant palm oil, Unilever is back in the news for falsely claiming to phase out single-use detergent packets. The company claims it's a "complex problem." Bullshit. The company's more concerned with protecting revenues than solving problems that it can instead leave for others to clean up. (Reuters)

Sunscreen kills coral. The problem is so severe that Hawaii banned most common sunscreens. But until recently, we didn't know why. A group of scientists determined that Oxybenzone, a sunscreen ingredient that blocks UV radiation, is metabolized into toxic radicals by corals, anemones, and coral symbiotic algae. Understanding the mechanism is the first step to creating a better sunscreen. (FreeThink*)

Good enough that I now have a jar of heavy pineapple syrup in the freezer to make more.

1.0oz Pierre Ferrand 1840 Cognac

1.0oz Plantation Stiggins' Fancy Pineapple Rum

0.75oz Lime Juice

0.5oz Rich Pineapple Syrup

1 dash Angostura Bitters

Pour everything into a shaker. Add ice until it comes up over the liquid. Shake for ~20 seconds, until the outside of the shaker is frosted. Strain into a coupe glass and enjoy!

I challenge you to find someone who dislikes this drink. It's summery pineapple without being too sweet. It's alcohol-forward without being overwhelming. It's got just a hint of spice from the bitters, a nod to its punch origins without forgetting the daiquiri base. Traditionally made with Jamaican rum, I opted for pineapple. And please don't knock it - I know what you're thinking but this isn't that. Plantation Stiggins' Fancy Pineapple Rum is made by infusing Queen Victoria pineapple rinds before distillation, imparting the oils without any of that sickly sweetness normally associated with pineapple rum. I'm hesitant to use it in cocktails - I normally drink it on the rocks with just a lemon peel - and don't want to waste any on unfulfilling pursuits. It's a sign of just how good Ned King's Gem is - I'll gladly use up the whole bottle.

Cheers,

Jared