Beyond the headlines, with a longer-term perspective, today's doom and gloom provides as many opportunities as it does hardships.

Hey friends -

Take one look at the headlines on any given day and you can be forgiven for thinking the world's going to come to an end. Inflation is high and seemingly rising. Russia continues to perpetrate atrocities across Ukraine. Supply chains are a mess. The stock market is down and crypto is down further.

Leave your house to escape it all and the narrative is reinforced. Gas is over $5 a gallon, $7 if you live in California. Rents are through the roof. Groceries are expensive. Chips cost the same but the bags are half empty.

A thousand little things that would each only be a passing comment in good times. Today, it can feel like everything's broken.

But everything's not as bad as it seems. When you get beyond the headlines, there are many rays of hope. With a longer-term perspective, today's doom and gloom provides as many opportunities as it does hardships. It's about having a different frame of mind.

In this week's letter:

Averages, risk, and returns: how thinking different can change your outlook

Facts, figures, and links to keep you thinking over a drink

A New Orleans classic cocktail, the Hurricane

Total read time: 15 minutes, 3 seconds.

🚨Heads up - this letter will get cutoff in your email. Lots of images. Click the title up top to open it in a browser.

I've been spending a lot of time revisiting writings from the dot-com crash, The Great Financial Crisis, and other blowups in recent history. Much of my reading has been letters from Howard Marks, Warren Buffett, and Charlie Munger.

Marks in particular does a great job titling his letters, including "Bull Market Rhymes," "Safety First... But Where?," "You Can't Predict. You Can Prepare.," and "bubble.com." If I gave you no further commentary, I expect the titles alone would give you a good sense of what I've been up to.

It's material that I've read many, many times over. My copy of Howard Mark's The Most Important Thing is marked up to the point where I may have doubled the number of words in the book, I've recounted Buffett's many trades and anecdotes so many times that my dog now repeats them back to me, and I've just about memorized all of Munger's checklists. And still, I find I learn something new every time I reread them. With more frequency than I'd like, that also means relearning hard lessons like Marks's advice to "go for batting average, not home runs."

John Huber of Saber Capital summed up my approach to reading in a recent letter:

I got to thinking about how not only do we create a unique database in our minds based on the specific collection of material we study, but also how this code base is continuously getting updated every time we read something (or have a conversation, or join a meeting, or listen to a podcast, etc…).

And what’s interesting about this is because the mental database is constantly changing, you can actually read the same thing you’ve read previously (re-reading a book for example) and come away with a completely different understanding, sometimes even an opposing view from what you held before. I’ve noticed this numerous times, as I happen to (weirdly) like rereading the same books numerous times.

The reading has helped reground my thinking - that everything's not as bad as it seems. But before we get to the good news, let's wallow in the bad.

Tech might have gotten a little ahead of itself. Since the start of the year, we've seen 21,000 reported layoffs and many more hiring freezes. The impact becomes all the more remarkable when you look at it on a per company basis:

MasterClass: turns out people don't watch as much when they're no longer stuck at home. 20% of the company laid off.

Notarize: Zoom-based notaries "as a Service" aren't worth it when you can go in person. 25% of the company laid off.

BlockFi: crypto's not doing so hot. 20% of the company laid off.

Coinbase: the US publicly listed crypto exchange. 18% of the company laid off.

OneTrust: cybersecurity tech. 950 people were cut in response to "capital markets sentiment" despite "record growth." 25% of the company laid off.

Peloton: no list would be complete without it. 20% of the company laid off.

Crunchbase is keeping an up-to-date list as more tech companies make similar announcements.

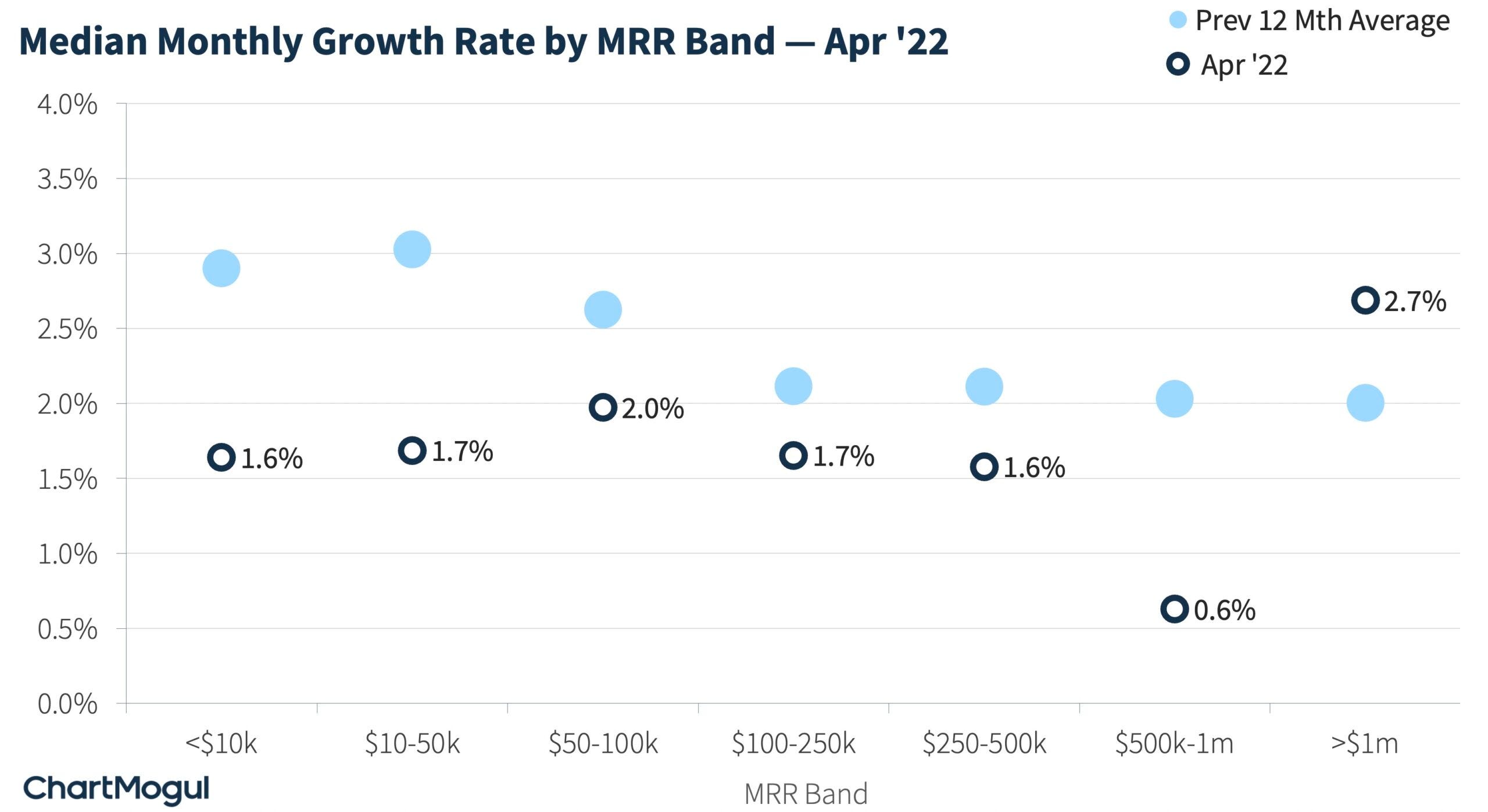

The layoffs follow reduce growth and growth expectations. ChartMogul, an analytics platform for SaaS companies, published a recent blog that details the carnage.

Note the two different trends. Not only was April revenue growth slower than the previous year, most companies expected the upcoming month to be even worse. That's the type of outlook that leads to layoffs.

Inflation is... well. It's ugly.

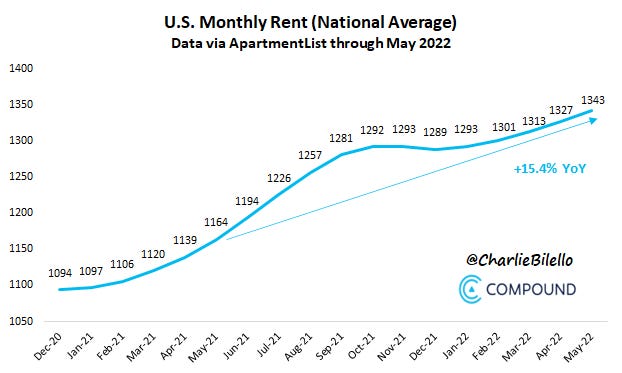

Housing costs are a third of the consumer price index. The official statistics likely understate the real rise in housing costs, a challenge we discussed in a previous letter. The cost of housing is likely outpacing overall inflation.

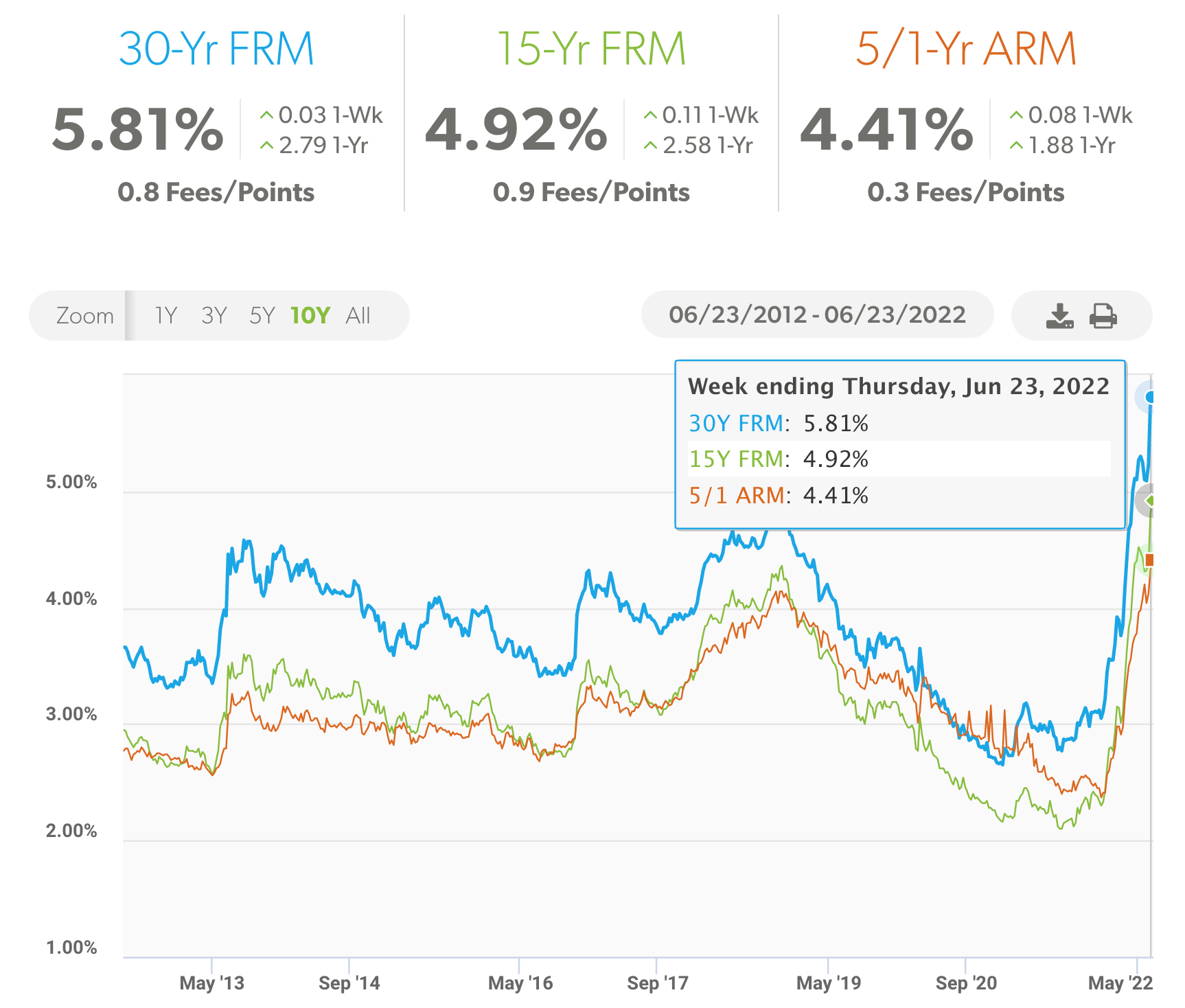

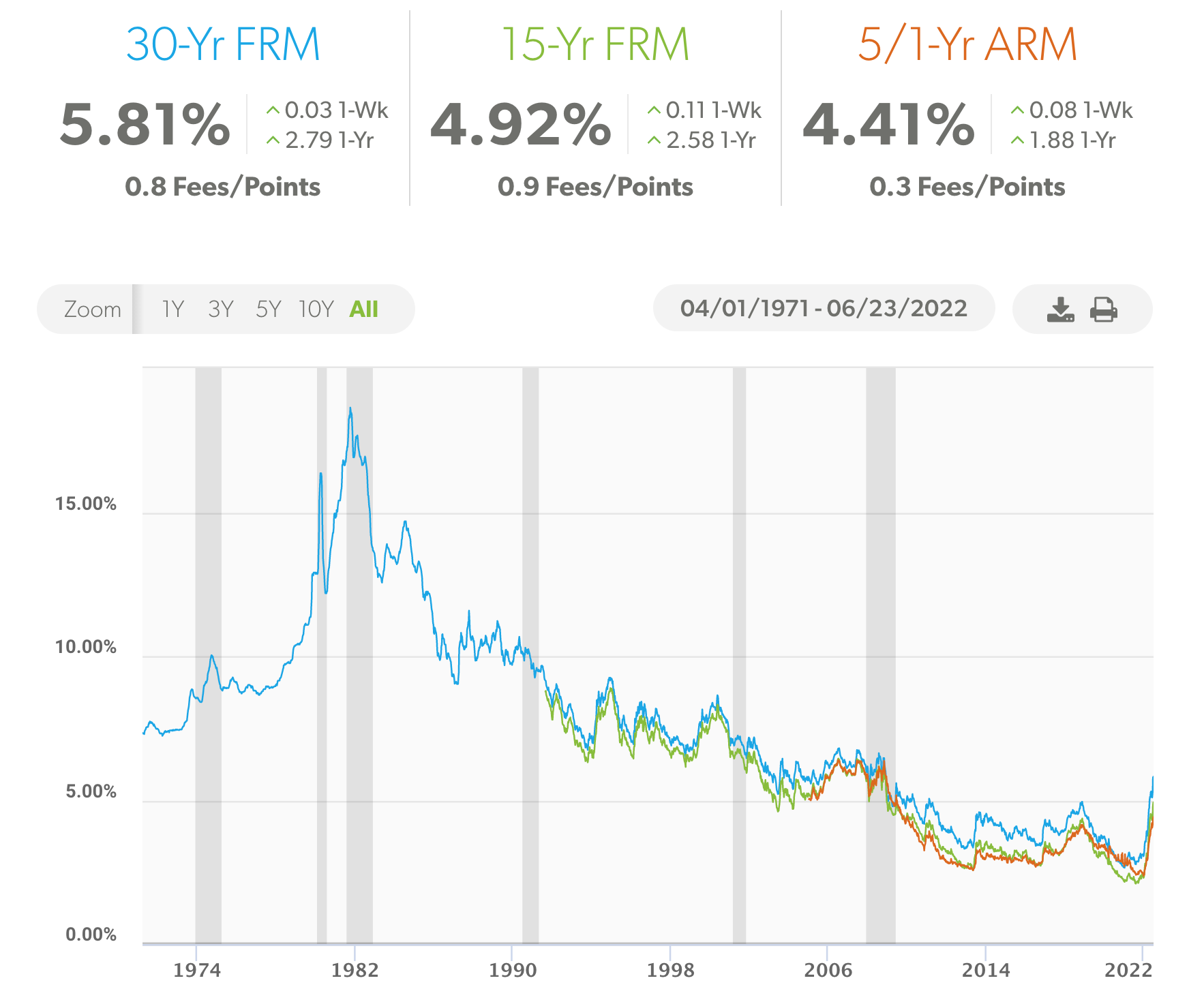

To add insult to injury, mortgage rates are increasing even as housing prices go up.

That massive jump in the past few months includes the week of June 8th which saw the largest one-week in mortgage rates since 1987. Translated into dollars and cents - new homeowners with a $400,000 mortgage are paying an additional $800 per month more than they would have paid had they taken out the mortgage this time last year.

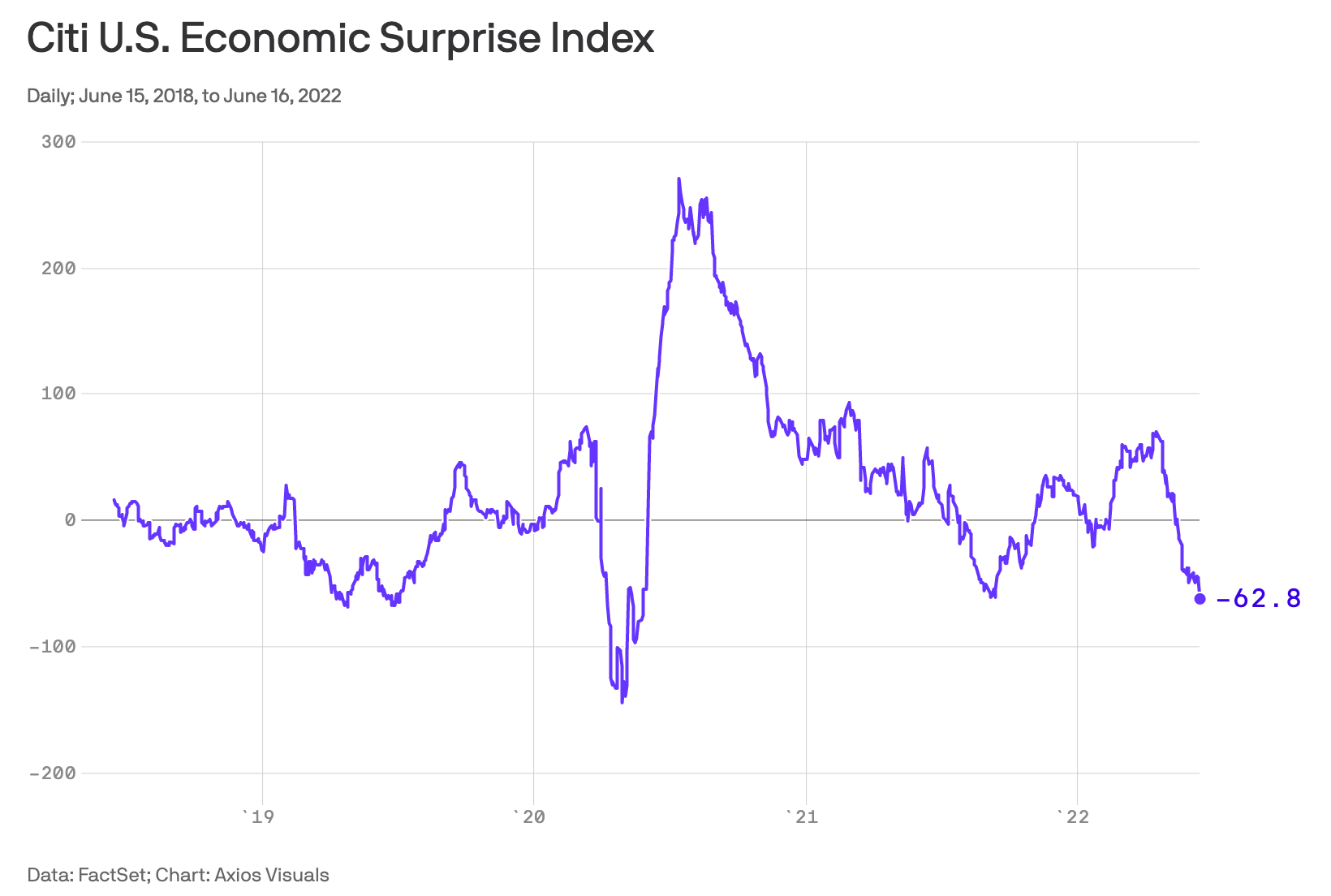

In case you were hoping we were getting better at predicting this stuff - don't hold your breath. Citi's Surprise Index measures how economic data compares with analyst predictions. We're still predicting rosier scenarios as economic data worsens.

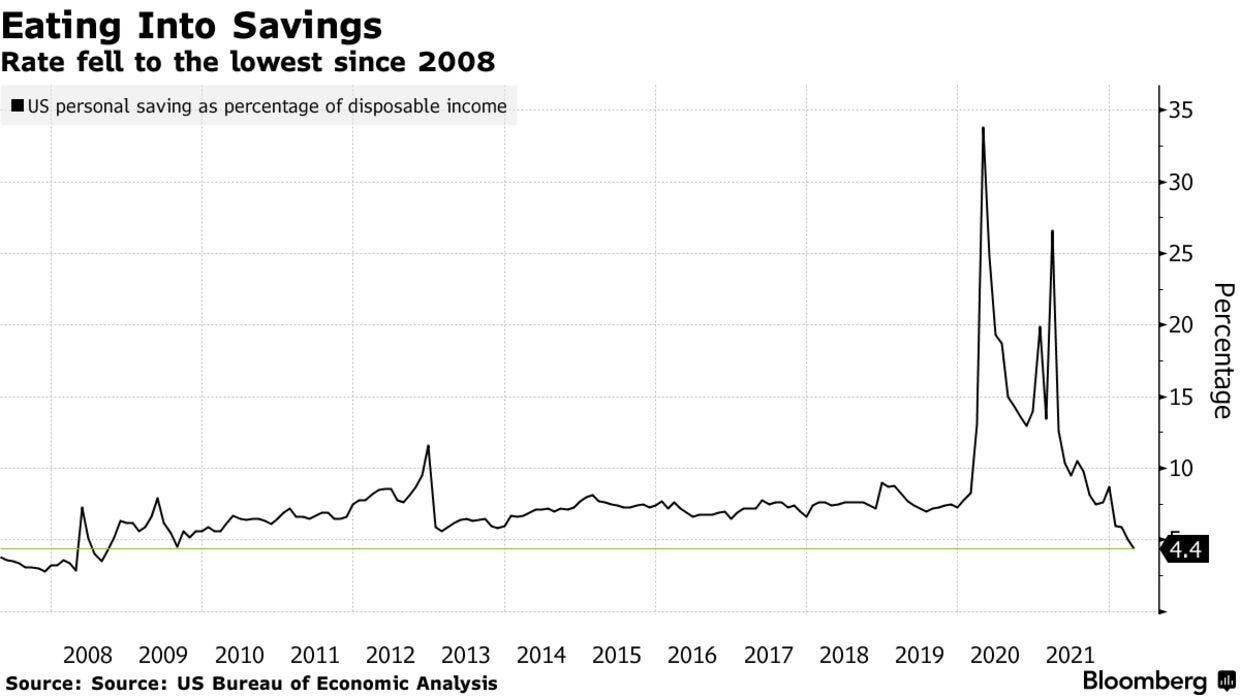

Every day consumers are taking a beating. We're spending more on housing, gas, and food and saving less. The still-falling savings rate is roughly where it was in 2008.

There's a lively ongoing debate as to whether consumer spending has fallen. It's an important conversation as roughly two-thirds of the country's economic activity is powered by consumer spending.

The data is mixed. There's little debate that spending has increased on gas and food - we consume about the same amount but prices have gone up. Spending on everything else is a more complex story. General retail sales have fallen slightly, and car sales fell 4% month over month in May, but spending at restaurants has remained robust.

The challenges of measuring spending patterns are compounded by a wealth effect - we spend less as we feel poorer from watching our net worth fall, such as when the value of our stock portfolio declines. But that reduced spend isn't spread evenly. We may choose to spend more on escapism experiences while still reducing overall spending.

Surprise, surprise. Supply chains are still a mess!

Inventory has been piling up at major retailers. The primary culprit? Unpredictable supply chains (emphasis mine).

Factory closures, shipping delays, port backlogs and other supply-chain bottlenecks wrought by the Covid-19 pandemic are prompting chains from Target Corp. to Gap Inc. to start designing new products and placing orders with overseas factories further in advance, making it harder to match supply with demand.

Production cycles—typically the time it takes to design products such as apparel and footwear and have them hit shelves—are stretching to over a year, up from about eight months before the pandemic, according to industry executives and analysts.

It's gotten so bad that Target and others are massively discounting inventory - essentially paying customers to move out-of-season goods out of their stores.

The story is no better with vehicle manufacturing. Elon Musk described the new Tesla auto factories in Austin, Texas and Berlin as "gigantic money furnaces" because of a shortage of batteries and China port issues. The CEO of Daimler Trucks, the largest truck manufacturer in the world, said it was "one of the worst years ever in my long [25-year] career in trucking" for parts shortages.

Not wanting to miss out on the fun, Toyota reduced its projected annual car production by 20% in March. And then reduced the June projections by 100,000 vehicles at the end of May. And then reduced June projections again just two days later by another 50,000 vehicles. All are related to the seemingly never-ending semiconductor shortage.

It's not just the big companies. Even a small boat-building school in Arundel, Maine is struggling with getting ship-building materials in time to teach this year's students.

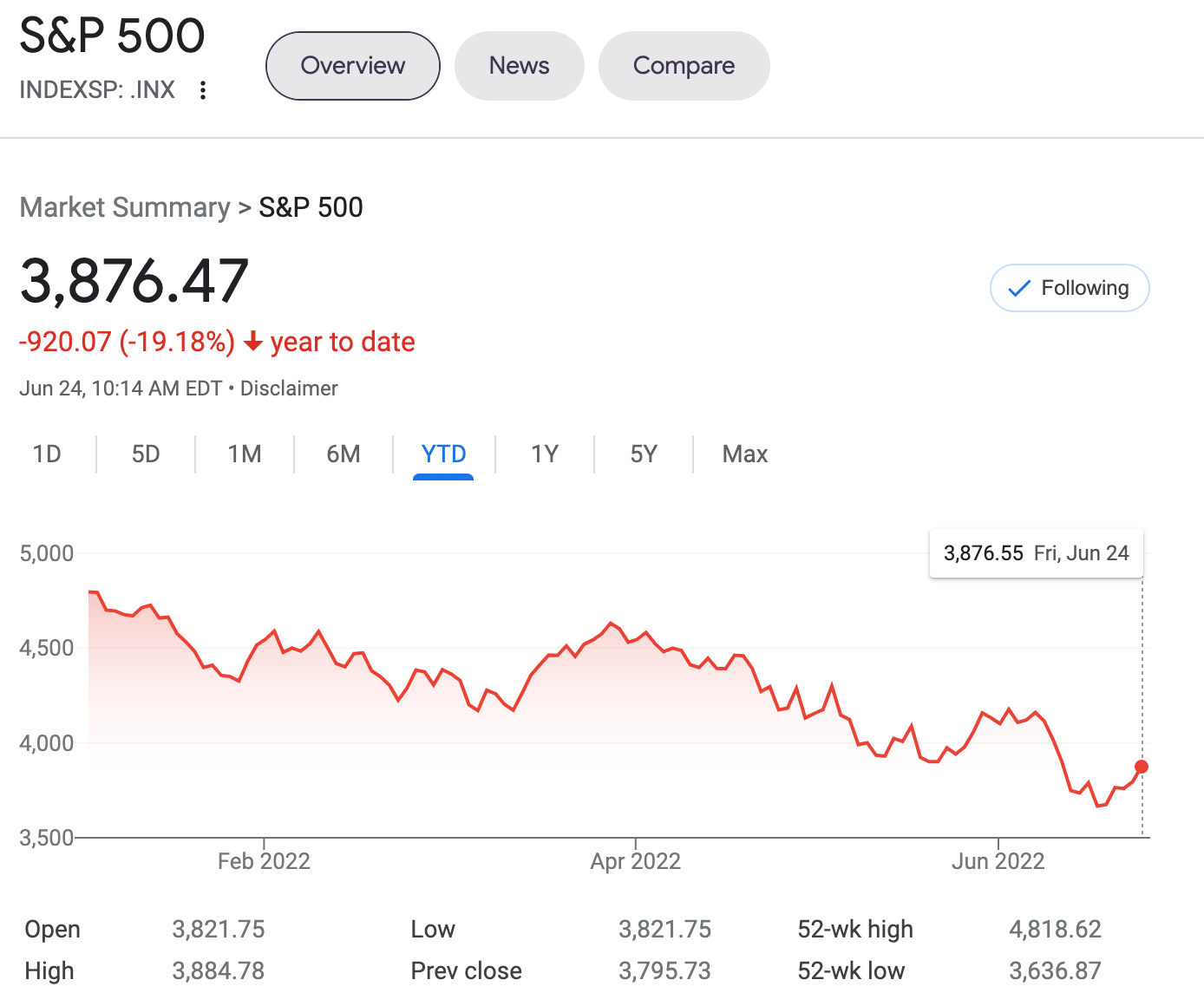

The stock market's down. It "officially" became a bear market as the S&P 500 fell more than 20% off its all-time high earlier this year.

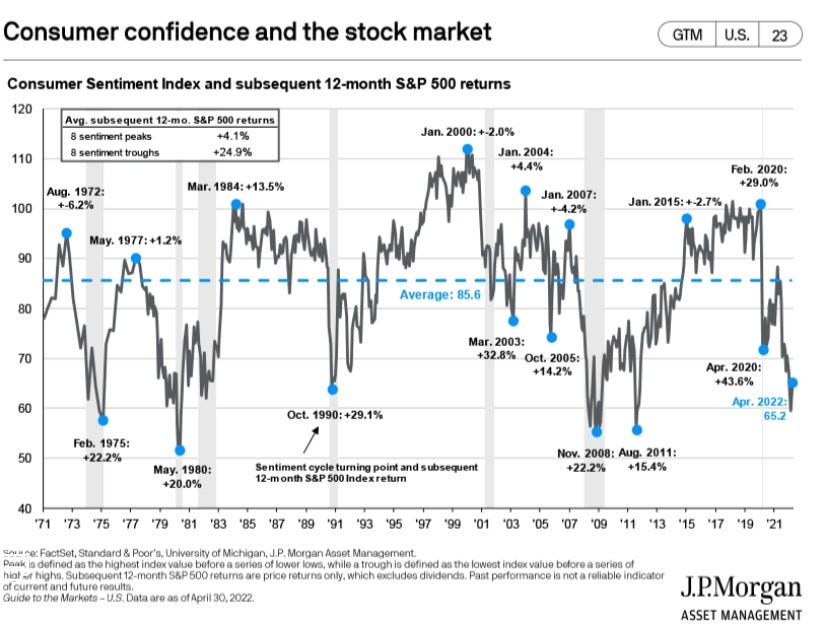

But what's interesting is that it feels down a lot more. Consumer confidence in the stock market is about as low as it's ever been since 1971, on par with the mid-1970s and late 1990, and only marginally better than the depths of 2008.

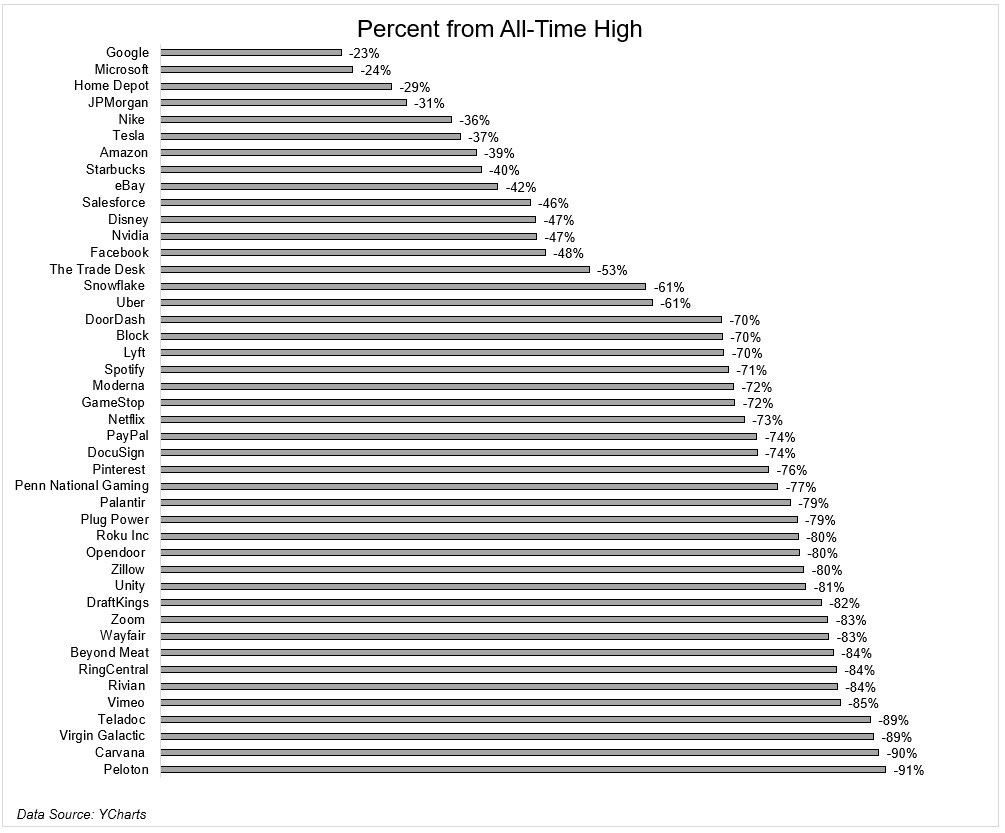

What's likely driving the divergence between sentiment and overall market performance is the makeup of that performance. Many of the most prominent public companies are down much more than the market average. It's not just the high-flyers like Tesla and Amazon, stalwarts like JP Morgan and Disney are down materially from their all-time highs.

The 20% fall in the stock market looks like child's play to the ongoing carnage in crypto.

The two largest cryptocurrencies by market cap - Bitcoin and Ether - are off more than 60% and 75% from their respective all-time highs in November 2021. The overall market size for all cryptocurrencies collapsed from $3 trillion to less than $1 trillion in that same period.

The rapid price decline has led to a series of seemingly never-ending bankruptcies as unhedged, debt-laden bets on price appreciation turned sour. The high-profile, multi-billion dollar blowups include:

TerraUSD - a supposedly algorithmically balanced "stablecoin" collapsed to almost nothing, leaving holders with over $40 billion in losses. In theory, fancy math and magic were supposed to keep the crypto pegged to $1 USD.

Tether - the largest "stablecoin" by market cap broke its peg to $1 USD. It's since recovered but continues to trade at a discount. Tether has notoriously refused to release any reasonable audit of what backs the token so it's anyone's guess what happens if there's a full-blown run.

Celsius - a centralized trading, lending, and generally multi-purpose crypto app is seemingly insolvent. The company raised over $864 million of venture capital funding and at one point custodied over $3 billion of funds for over one million customers. It's halted all redemptions, meaning users cannot get their money out.

Three Arrows - a multibillion-dollar family office / hedge fund just failed to meet multiple margin calls and is supposedly refusing to respond to creditors. That means they're in default. It's as-yet unclear if the entire firm will go under, but it appears likely.

Voyager - a publicly listed crypto company (VOYG.TO) lent $660 million to Three Arrows and now likely won't get paid back. The company reduced the daily amount that customers can withdraw from $25,000 to $10,000 and borrowed over $500 million from Alameda Research to try to stay afloat.

I think that's probably enough. I could go on, but you probably get the picture at this point. It kind of seems like we're going to hell in a handbasket.

But if there are doomsayers among you, I'll happily take the other side of the bet. You just have to allow me a reasonable time horizon.

Things aren't that bad, or at least they could be a lot worse. And they're going to be a lot better in the future.

This isn't about being hopeful or optimistic. It's about recognizing that the world moves in cycles, taking a longer-term view, and making a bet that the cycles will continue. I'm just as certain that the boom times will return as I am that they'll be followed by more busts.

That's not to say things can't get worse first. But I have no particular aptitude for precisely pinpointing the bottom. I'm much more comfortable looking out over years and decades and betting on the long-term trends.

Let's put into perspective each of the supposedly bad scenarios.

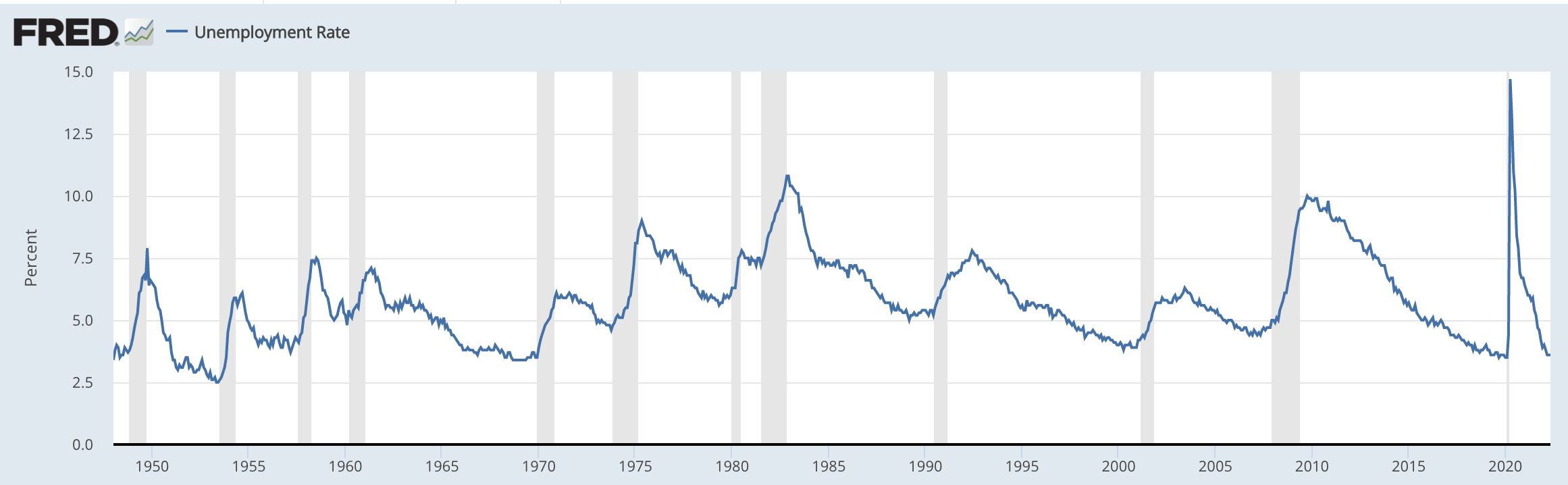

The unemployment rate is as low as it's ever been since the late 1960s. You have to go all the way back to the early 50s, just after World War II, to find anything lower.

While that may be little comfort to laid-off tech employees, we also can't really understand tech layoffs without better knowledge of the base rate. In "normal" times, what is the annual employee turnover for a rapidly growing tech company?

Tomasz Tunguz, a venture capitalist at Redpoint, assembled the data. LinkedIn crunched their own data for 2017 and discovered a 13% turnover rate for tech and 10% overall. Founders Circle, another venture capital firm, surveyed hyper-growth startups and discovered that average employee tenure was no more than two years, leading to a surprisingly high 25% turnover every year.

Go back to the headline layoff numbers - 20% here, 25% there. Well within the expected range for a fast-growing startup. Absent the base rate, layoffs seem remarkable. With it, they become a non-event.

Inflation expectations appear to already be trending lower. Per Bloomberg:

The University of Michigan’s final June reading of longer-term US consumer inflation expectations settled back from an initially reported 14-year high, potentially reducing the urgency for steeper Federal Reserve interest-rate hikes.

Respondents said they expect inflation to rise 3.1% over the next five to 10 years, down from a preliminary reading of 3.3%, according to Friday’s report. They see prices advancing 5.3% over the next year, matching the initial figure.

The Federal Reserve's recent and large 75 basis point increase in the benchmark interest rate likely helped. It's not just the immediate effect, it's that the Fed is signaling that it will do what it takes to reign in inflation. Realized inflation is as much about expectations as it is about what happening right now. Changing expectations really does change inflation.

Let's also put that housing cost into perspective. Yes, mortgage rates are going up. But they remain unbelievably low by historical standards.

That means relatively to equity, homes are still cheap to buy. And unlike in 2008, most households have a lot of income relative to mortgage payments. Mortgage payments are just 9% of income, lower than it's been since 1980. That puts homeowners in a much stronger position to keep their homes even in home prices come down.

It appears that the housing market is cooling off. The National Association of Realtors noted that we have 2.6 months of housing supply for sale, meaning it would take that many months to sell all the homes currently listed. That's lower than the healthy four-to-six months supply, but a 33% increase over February.

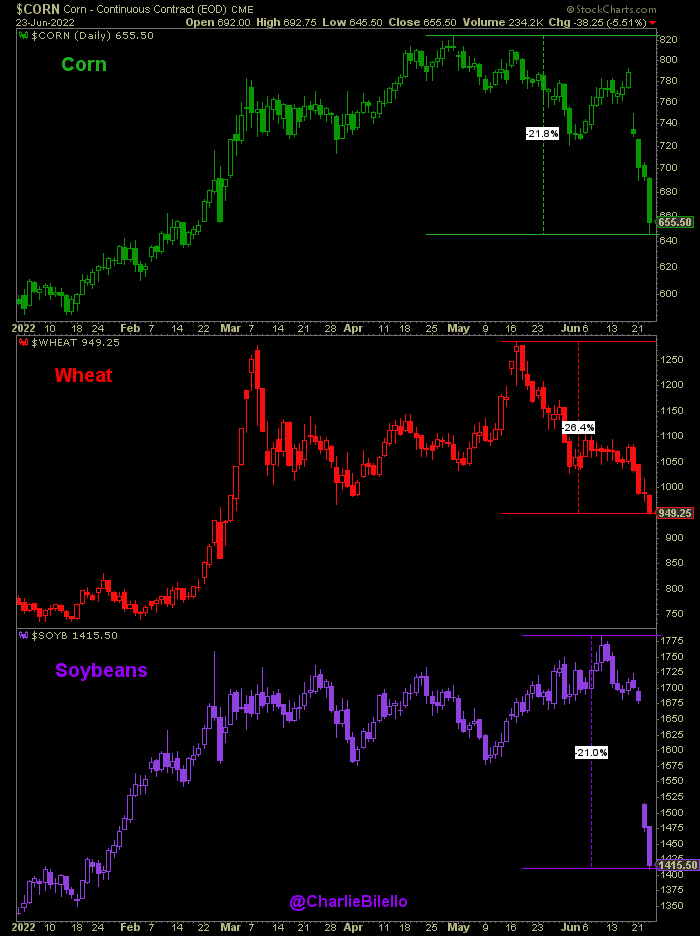

We're also seeing food prices start to come down. The prices for corn, wheat, and soybeans - the main foodstuffs in the US - are all down more than 20% from their recent highs.

Prices remain elevated relative to historical norms, but they're unlikely to form a "new normal." Corn is the largest by volume. Consumption has increased about 3% a year for the past 30 years, a 120% cumulative increase, yet the current price is about three times what it was 30 years ago and twice what it was for much of the past decade. More likely than not, we'll return to foodstuffs prices in line with historical norms.

Inflation is still very real, but we're seeing the tide turn for two key inputs - housing and food.

We may be through the worst on supply chain issues as well.

Freight rates - the cost to transport shipping containers - between China and the West Coast appear to be coming back to earth.

It's a trend that reflects the much-improved wait times for the container ships themselves.

We're slowly but surely moving more stuff, faster, and at cheaper rates. That doesn't mean it's all smooth sailing back to normal operations, but we're nonetheless making steady incremental improvements.

It's a similar story for semiconductors, the worst seems to be behind us. Texas Instruments, the leading maker of analog chips, advised its clients that shortages will ease in the second half of this year. Samsung, a massive consumer of semiconductor chips, is "temporarily halting new procurement orders."

Turns out, businesses ordered a lot of chips! More than they could actually use and now many are sitting on excess supply.

If we look at out even further, there are tremendous ongoing investments in new chip fabrication that will materially increase production.

Not only are the current challenges starting to alleviate, but we're also already investing billions of dollars to head off future shortages too.

Let's jump to the punchline first. From Long & Short of Stock Performance:

Taken as a whole, these drivers collectively will continue to underpin strong US performance on the global scale for years to come... It seems more probable than not that the US will continue to be the world leader and that its growth will translate to attractive stock market returns over the long run.

Nothing's changed in that regard.

While the market bounces around, it helps to keep in mind the funkiness of annual returns:

Over 40% of the years saw positive or negative returns greater than 20%

About 50% of the years in which returns were negative saw a loss of more than 10%

Returns in almost 75% of the years were positive

That covers almost 100 years of the US stock market.

What changes in the short term is sentiment. We alternate between wildly excited and inconsolably pessimistic about the prospects of companies. But the companies themselves don't change course anywhere near as rapidly as our emotions do. Tesla, Amazon, JP Morgan, Disney, and almost any other company you can list is largely the same as it was six-plus months ago when the price was higher.

But the price has changed and that's a good thing. I get excited when I find that the liquor store is having a sale on High West Double Rye!. I spend less money to get the same great value. Just a few paragraphs earlier, I was celebrating that prices for housing, foodstuffs, and freight are all coming down.

Shares in companies are no different. When they go on sale, you get the same great company for less. As John Huber recently stated, "the simple fact is that when you’re buying something, you should prefer a lower price."

Does that help you feel better in the short term? Probably not. You feel poorer as you watch your retirement account get momentarily smaller. But that's life. Charlie Munger put that dose of reality best in 2002:

If you’re going to invest in stocks for the long-term, or real estate, of course, there are going to be periods when there’s a lot of agony and in other periods when there’s a boom. And I think you just have to learn to live through them.

The same thing that holds true for stocks holds true for crypto. If you're buying something, you should prefer a lower price.

An additional note of caution is warranted. Not on crypto specifically, but on leverage. Despite all the hubbub about how crypto will reinvent finance, every insolvency I cataloged happened from the same poor decision making.

Leverage - using borrowed money to make investments - does not change the nature of returns, it only amplifies them. As surely as it will increase gains as prices rise, it'll increase losses as prices fall.

Celsius offered 8% yields and TerraUSD offered 20%+ at a time when the risk-free rate from the US Government was less than 2% even if you lent the government money for 10 years. The only probable way they could generate those returns is through fraud or leverage.

There are many promising crypto projects with real user bases consuming real products that deliver real value. There's no mystery about how they make money. Many of them are now are sale.

I don't know. And I'm okay with that.

Yes. Looked at through one lens, the one that shows up in the headlines and on TV, the world's not in great shape. It's easy to find yourself mired in misery.

No. It's not the only lens. Through another, one that takes a longer-term perspective where boom and bust cycles come and go as surely as the side, the world's doing what it always has. The sun will rise again tomorrow and the good times will return.

What happens between here and there? We'll see. There are bright spots among the gloom that portend better days at hand, but they may simply be false hope.

But me? I take comfort in the long-term perspective. I intend to be around for many years to come. With that as my horizon, I find that everything's not as bad as it seems.

A new paper documents the effect of the 1970s rapid increase in the price of gas on long-term driving habits. Short version - people drive a lot less. But there are fascinating nuances to further explore: "individuals respond to price changes during their formative driving years much more so than to price levels." It's a particularly topical paper as we consider the long-term effects of current inflation. (Web3 Breakdowns)

One of the best articulations of how NFTs and crypto can unlock new forms of customer interaction from none other than Shopify's Alex Danco. This is more than just talk - Alex is building tokengated commerce reality Shopify. (Curbed)

Hoboken has had zero traffic deaths since 2018. While any such statistic given in isolation should be taken with a grain of salt (Hoboken may just have gotten lucky), it seems that there is more than just an element of luck here. The city has been systematically redesigning roads and intersections to increase visibility and reduce the likelihood that encounters are fatal. In a country where traffic fatalities remain a leading cause of death, there's much to be learned. (Science)

The stunning Spix's macaw, a brilliantly blue-grey parrot, is poised for reintroduction to its native Brazilian habitat twenty years after the last wild member of its species died. It's a story full of hope for the successful rebirth of a wonderful species. (Wharton)

This one always makes me smile.

2.0oz Overproof Potstill Rum

1.0oz Passionfruit Syrup

1.0oz Lemon Juice

Pour everything into a shaker. Add ice until it comes up over the liquid. Shake for ~20 seconds, until the outside of the shaker is frosted. Add crushed ice to a Hurricane glass. Strain into the glass. Top with more crushed ice as needed until it comes up to the rim of the glass. Garishly garnish.

Are there better drinks? Definitely. Are there better versions of the Hurricane? Absolutely. Is it even a good drink? Honestly, not really. But it makes me smile every time and that’s half the fun. The passionfruit is entirely too much and lemon is far my from go-to citrus pairing with potstill rum. It’s a drink that was made to get you drunk - the original recipe is a double serving - on the streets of New Orleans in the heat summer. Enjoy it not because it’s good (it’s not), but for the absurdity of it all.

Cheers,

Jared