Apple announced Apple Pay Later, a buy now, pay later service. Left unannounced was how they'll deal with collections.

Hey friends -

Apple recently launched Apple Pay Later, a Buy Now, Pay Later service through Apple Pay. That made headlines.

What didn't make headlines was the real story. Apple itself - not a partner - is operating the service. No bank, no financial services partner, just Apple.

So what happens if you default, if you fail to "pay later?" Apple Debt Collections™️.

In this week's letter:

Apple Debt Collections: discovering what it means to be a financial services company.

Right to repair, breathing through your butt, and more cocktail talk

A multipart cocktail series, starting with the crisp and clean Daiquiri

Total read time: 10 minutes, 44 seconds.

Unbundling the full extent of Apple's fintech services is a doozy.

Most of the headlines have been about the Apple <> Goldman Sachs partnership for the Apple Card, an Apple-branded credit card on the Mastercard network issued by Goldman Sachs. But that's by no means the only partnership. Here's a smattering of other, still live engagements:

Apple Cash, powered by Greed Dot Bank. Apple Cash is a virtual cash account that lives in your Apple Wallet and allows you to instantly transfer money similar to how Venmo works. You can move money between friends, send it to businesses, or transfer it to your bank account. Formally it's called Direct Payments.

iPhone Installment Loan, powered by Citizens. When you purchase a new iPhone and choose to pay for it monthly instead of upfront, that's an installment loan. The loan is underwritten by Citizens Bank.

AppleCare and AppleCare with Theft and Loss, powered by AIG. The insurance program for iPhones is underwritten by AIG. It's a shift from previous underwriter Assurant as of September 2020.

Across all of the engagements, Apple partnered for financial services. There are a couple of notable exceptions where Apple in-housed the services through subsidiaries including Apple Gift Cards issued by Apple Value Services, LLC and AppleCare+ underwritten by AppleCare Service Company, Inc.

But gift cards and technical support services are fairly vanilla as far as financial services go. Apple Pay Later is a step in an entirely different direction. A wholly owned subsidiary, Apple Financing LLC, will be the lender. It's a shot across the bow of the company's partner banks.

Not that it's been able to rid itself of bank partners entirely. A quick look under the covers of how buy now, pay later works shows why.

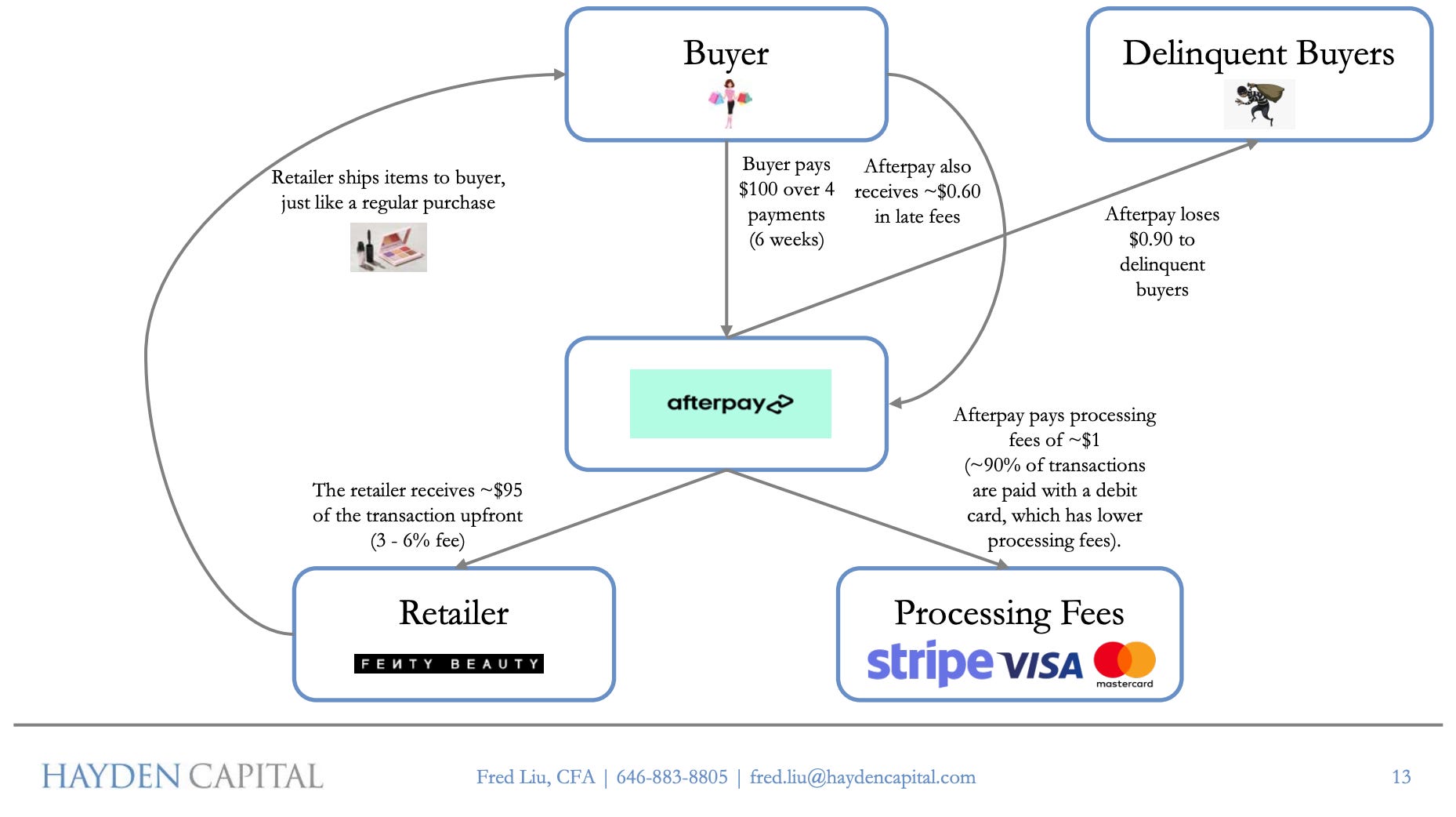

Think of buy now, pay later (BNPL) as an alternative to a credit card - it's a short-term loan so you can defer full payment on a purchase.

The standard BNPL setup is Pay in 4. Your purchase is split into four equal payments over six weeks: you pay 25% upfront and another 25% every two weeks until the full amount is paid off. It's a zero interest, zero fee loan as long you pay on time.

Under the covers, the merchant foots the bill. When they agree to accept BNPL, they also agree to share ~5% of the gross revenue with the BNPL firm. That's about double what they pay if they accept a credit card.

One more critical difference - the payment flow is rewired so the BNPL company is the primary interface with the merchant and with the consumer. When a customer uses BNPL, the BNPL firm pays the merchant and the customer pays back the BNPL firm.

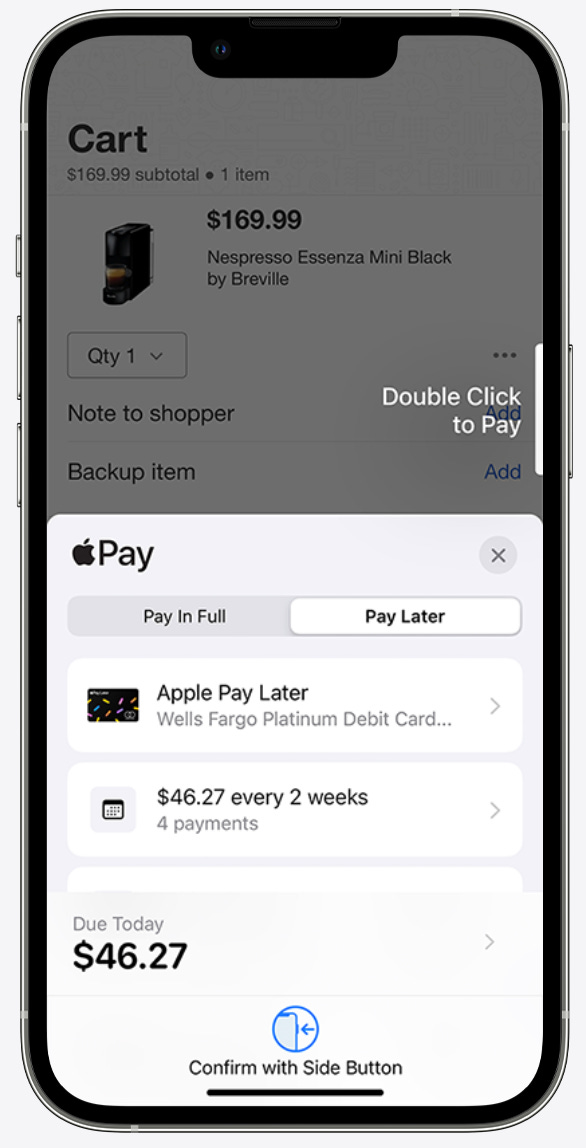

Like most BNPL offerings, Apple Pay Later is a zero-interest, pay-in-four scheme. Purchases will be capped at $1000. Apple, as the lender, will determine creditworthiness through whatever data they have on you but without a hard credit check. Everything happens through the Apple Wallet including automatic repayment via a user's linked checking accounting.

The model is all well and good, but you still need a way to actually make those four payments. Apple, even as a lender, cannot issue a card that can use the Mastercard payment network. Apple still needs a banking partner - Goldman Sachs. The bank will issue virtual debit cards, held in users' Apple Wallets, to actually facilitate the payments.

There's not a lot much more to it. It's yet another BNPL offering among the more than sixty-seven that Pymnts.com has inventoried.

The key question for me is what happens if you don't pay back your loan. What does Apple do?

Before we entirely move off Goldman, it's worth noting that this is all fairly novel for the bank. While we've called Goldman a bank for many years, that's not entirely accurate. Before the Great Financial Crisis, the "bank" only held a license as an industrial loan company. While that is technically a banking license, it's more banking-lite. Among other restrictions, because Goldman had more than $100 million in assets, it could not offer consume demand deposits like checking accounts.

Goldman only converted to a bank holding company with more robust banking subsidiaries during the Great Financial Crisis. The switch was a prerequisite to the firm receiving Federal Reserve bailout money - the Fed couldn't directly inject funds into a state-regulated industrial bank that lacked a Federal Reserve Master Account.

The bank put the new license to good use in 2016 with the launch of Marcus by Goldman Sachs, a digital-only consumer bank. The bank has since scaled to 10's of billions in consumer deposits, billions in loans, and millions of users. The Apple <> Goldman relationship is an extension of Marcus. Not bad for a 6-year-old bank.

Apple states on its website that the six-week installment loans are "with no interest or fees to pay." CNBC reports that the company won't report missed payments to credit bureaus. I'll believe it when I see it. The official terms and conditions for Pay Later are not yet published.

There's inevitably a collections process for loans in default. These are loans, not grants. You can't lend money and simply hope users pay it back.

Apple is highly likely to keep collections in-house. A major reason for lending off of Apple's balance sheet was to "avoid sharing personal data with third parties." Outsourcing collections would pose the same challenge.

It puts the company in a particularly thorny spot. The Consumer Financial Protection Bureau recently launched an invite-only club for the major BNPL providers in the US to investigate "systemic, underlying problems." It's odd to find Apple pounding the table to join.

But for me, that's the sideshow. Regulated financial services providers land themselves in hot water with regulators because they've failed - or seemingly failed - to appropriately engage consumers. That can include everything from not disclosing terms and fees to abusing consumers during the collections process.

The key question is what it means for the Apple brand. What does it mean when the consumer starts to think of Apple the lender or Apple the debt collector rather than Apple the product company?

Forbes puts Apple as the #1 most valuable brand.

You'll notice a certain type of company is missing from the top-15 list - financial services. You have to scroll down to #18 to find Visa and all the way down to #45 to find the first bank, JP Morgan. It's not until you get to #67 that you find PayPal, the first standalone consumer-facing financial company.

We find similar results with Net Promoter Scores, a way of measuring how likely consumers are to recommend a product to a friend. Apple scores a 54 with just 14% of users listing themselves as "Detractors." American Express, the top-ranked financial services company scores just a 29 with 28% of users as detractors. PayPal's scores just a 15.

Affirm, one of the largest BNPL competitors in the US, has an NPS score of just 12 with 38% of users listed as detractors. The other BNPL firms aren't any better.

As the premier brand, Apple has a lot to lose. No matter how well Apple delivers the Pay Later service, they're associating the brand with activities that are clearly less favorable in the consumer's mind. The downside risk seems extraordinarily high.

Take credit cards for instance. I have little allegiance to Visa, Mastercard, Amex, or Discover. When my card doesn't work, such as when a charge is paused due to suspected fraud, I find myself annoyed with the card issuer - Chase, Fidelity, or the like. I associate the card with the issuer whose logo is front and center, even though many of my grievances are due to the underlying card network.

That said, my credit card usually just works. I'm not particularly enthusiastic about any of the issuers but you can be damn sure I throw a fit when I'm stuck in yet another phone tree trying to resolve a problem. The upside brand affiliation is limited but the downside is huge.

Apple's done a decent job protecting the brand with AppleCare. Customers continue to associate Apple with a new phone but blame the partner insurer for the process of getting it:

"This feels like a huge scam on the part of AIG."

"I agree that communication and customer experience with AIG are terrible."

"I have been on the phone with this company (AIG) for hours!!!"

"AIG is a crap company that does everything possible to make the process slow, painful."

But what happens when there's no longer a fintech partner to blame?

Instead, it's just Apple on the other side of the process trying to help resolve a situation. At best, Apple retains its beloved status. More likely, Apple comes to represent something negative.

Collections is among the most difficult businesses in which to maintain a good reputation.

To say collections has a bad reputation gives the industry too much credit. It's the #1 source of fraud complaints to the Federal Trade Commission and the #2 source of complaints to the Consumer Financial Protection Bureau (CFPB).

It's an industry marred by old-school dial-for-dollars practices that focus more on harassing consumers into paying than it does on actually helping them get out of debt. On average, internal collections recover just 20% of delinquent debt.

There are notable exceptions. Summit Account Resolution, is a traditional people-based debt collector that focuses on "preserving human dignity." They successfully helped 12,700 consumers out of debt delinquency last year and recovered over $140 million since the company's founding in 1996. The success didn't come at the cost of abusing consumers - recovery rates are twice the industry average, complaints are just a fraction, and the company is Better Business Bureau accredited with a perfect A+ rating.

The challenge is that a business with a model like Summit's doesn't scale well, certainly not to the 101 million iPhone users in the US alone.

What does scale is technology. TrueAccord is the oldest and likely the largest fintech in the space. They've worked with over 24 million customers, all while maintaining a Net Promoter Score of 40, an A+ Better Business Bureau Rating, and 4.8 stars on Google Play. Almost unbelievably, it's a beloved brand even though it's a debt collector.

Despite the headlines about "going it alone" as a BNPL lender, I expect Apple will partner here too.

Apple won't simply write off unpaid debts. That's not a viable business model. Instead, just as it partnered with Goldman for the virtual debit cards because it doesn't want to be a bank, Apple will partner with TrueAccord or another fintech for debt collections.

It'll allow Apple to scale a personalized, empathetic collections service that works from an assumption that consumers want to pay back loans, but perhaps have fallen on hard times. Executed successfully, Apple can become almost a financial partner to its consumer. It's a position TrueAccord already finds itself in today with reviews like this:

It will still be an exceptionally high-risk endeavor for the company. The potential negative brand impact for Apple is significant, whether directly from consumers or indirectly from association with BNPL compatriots in the exclusive CFPB club. Pay Later will also raise yet more antitrust concerns unless the company opens up Apple Wallet to other BNPL service providers, a move it seems highly unlikely to make.

Given the risk-reward, I'm not entirely sure why Apple decided now was a good time to try BNPL. I'm nonetheless fascinated to see how it plays out. Apple Debt Collections™️ will be an astonishing new service.

Call me a fanboy - I love OXO. To take something as pedestrian as a peeler or a salad spinner and reinvent it, not for beauty but for function, it's for me the pinnacle of design. To do so for almost every damn tool in the kitchen is incredible. There's an enormous amount to be learned from a company that executes on the ordinary so extraordinarily well. (Slate)

Right to repair is finally making meaningful headway. We've been under an unquestionable oppressive and likely unconstitutional Digital Rights Management regime since the Digital Millennium Copyright Act in 1998. While overpaying for an "official" iPhone repair may be just an expensive annoyance, imagine being immobile and waiting eight weeks and paying $300 to replace a $6 inner tube in a wheelchair. The time is ripe for change. (EFF)

File this under "Thomas Malthus Got It Wrong, Part 372." It appears we - the world - passed peak agricultural land use around the year 2000. While food production continues to increase, the land used continues to decline. It raises a particularly enticing opportunity as we explore ways to rebuild biodiversity - what should we do with all the extra land? (Our World In Data)

Many years ago, when I was probably supposed to be doing something far more productive, I got into a discussion with a friend about what would theoretically be the fastest way to get drunk. Our science teacher overheard the conversation and volunteered a suggestion that I've never tested but also never forgotten: dry ice, a hookah, and an orifice more frequently used for disposal than intake. Fast forward to a recent headline in Science: "Mammals can breath through their intestines: new study suggests anal ventilation might one day help treat respiratory failure." Fancy that. (Science)

A too often overshadowed classic.

2.0oz Aged White Rum

1.0oz Lime Juice

0.5oz Coconut Sugar Simple Syrup

Pour everything into a shaker. Add ice until it comes up over the liquid. Shake for ~20 seconds, until the outside of the shaker is frosted. Strain into a coupe glass and enjoy!

Simplicity at its finest. With the endless variations on the Daiquiri, the original sometimes gets forgotten. It's too bad. It's a wonderfully crisp, clean drink that takes little-to-no effort and can be rejiggered to the imbiber's preference. I already played around just a little. The original calls for un-aged white rum and simple syrup, flavors a bit too one-note for my tastes. Aged rum and coconut sugar bring a hint of dirtiness to the equation with the same molasses flavors that give rye, gingerbread, and carrot cake a depth to their sweetness. But you could go a different direction entirely - omit the sweetness entirely to play up that back-of-the-mouth citrus from the lime. Go real crazy to create the Ti' Punch, the national cocktail of Martinique and Guadeloupe. It's two ounces of Rhum Agricole, a teaspoon of sugar cane syrup, and a lime coin - just the circle butt-end of a lime - served as a scaffa, a room temperature drink that never touches ice.

There's lots of fun to be had with the Daiquiri, everything from the Hemingway Daiquiri to the 1800s Gem. The next couple of weeks will feature a number of my favorite variations. It's hard work, but someone's got to drink it.

Cheers,

Jared